")

Plains All American (NASDAQ:PAA) is a relatively large-scale MLP with a market cap of just over $12.5 billion. It owns and operates midstream energy infrastructure based in the United States and to a lesser degree in Canada. The main segments are pipeline transportation and storage of crude oil and NGL, where the crude oil accounts for the lion’s share of PAA’s EBITDA generation. For example, the operations that are associated with crude oil explain roughly 89% of the guided EBITDA for 2024. Also, from the CapEx side, the bulk of proceeds is directed towards the crude, thus sending a clear signal that PAA’s core business exposure is set to remain unchanged.

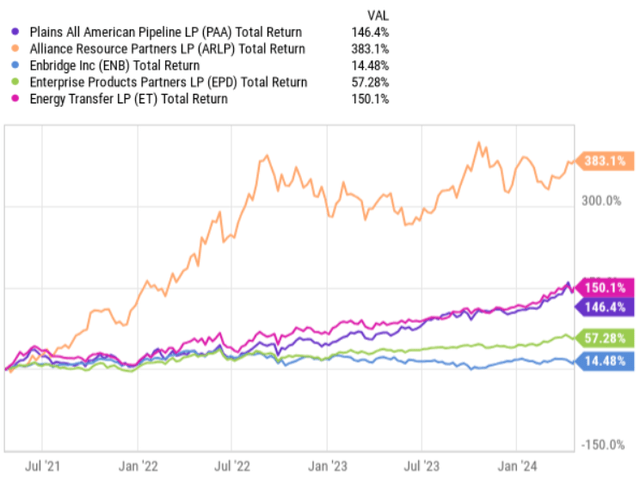

Now, if we compare PAA with some of its closest peers, including the broader midstream energy / MLP market as represented by the Alerian MLP ETF (NYSEARCA:AMLP), we will notice a huge alpha, where PAA has exceeded its benchmarks in a significant fashion.

YCharts

This theoretically might pose a question on whether PAA has not gotten too expensive and that perhaps that all of the upside has already been registered.

Here, we have to contextualize this with two nuances.

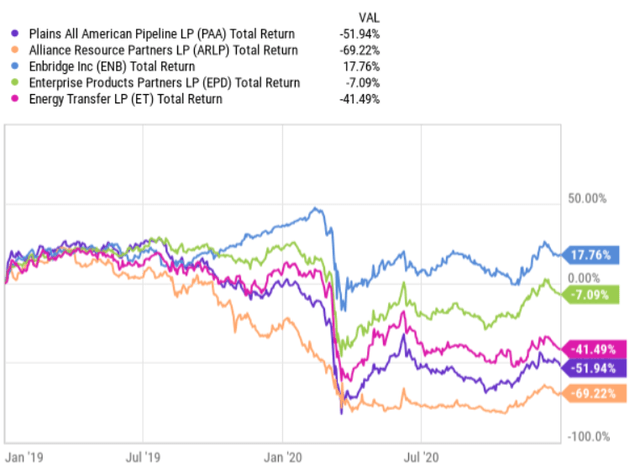

First, a major driver of the recent (3-year) outperformance by PAA has been the overall recovery process from a massive drop that PAA experienced during the early days of the pandemic. PAA suffered so badly because of an unfavorable timing, where the MLP had committed notable amounts of capital into new growth avenues, which made the balance sheet excessively indebted, weakening the Company’s financial profile to safely weather the Covid-19 related storm.

The chart below illustrates how actually at that time PAA was clearly the worst performing constituent of the stocks that were reflected above and which PAA has now outperformed in the past 3-year period.

YCharts

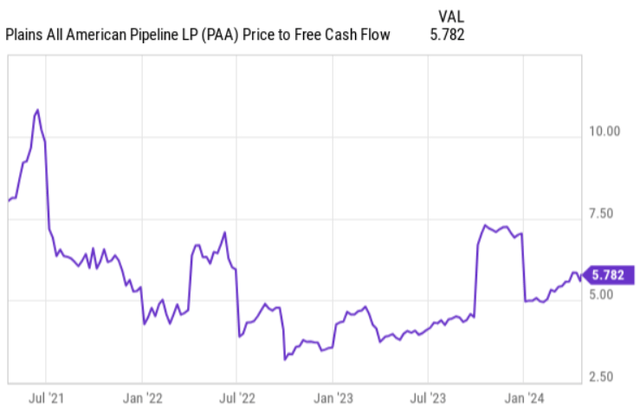

Second, although PAA has more than tripled in its value, on a price to free cash flow basis, the Company still seems fairly attractive with no signs of inflated metric.

YCharts

Now, once we have cleared the concern about PAA being too richly valued due to its solid 3-year price appreciation results, let me know elaborate on why I consider PAA an enticing buy at these levels.

Thesis

Besides the favorable dynamics that we can notice at the crude oil and the overall commodity end, I see several PAA-specific drivers that should warrant a continued outperformance of AMLP (i.e., the market) going forward.

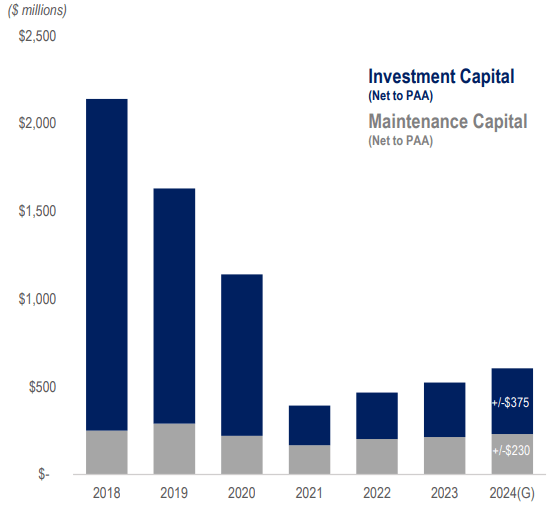

We have to appreciate that the CapEx heavy cycle for PAA is over, and that on a go forward basis, PAA will have to inject more moderate amounts of capital into both maintenance and organic growth opportunities.

PAA Investor Presentation

For instance, the total estimated CapEx for 2024 is at $600 million, which in the context of guided midrange in EBITDA generation of ~ $2.75 billion leaves PAA with a solid amount of internal cash generation to either de-risk the balance sheet or reward the shareholders directly through dividend distributions.

What this does is it also enables the Management to reduce the financial risk in the Company not only from the indebtedness perspective, but also from the committed capital angle, where such large CapEx amounts as before effectively narrowed the permissible margin of error in the underlying cash generation.

Already this year, we could notice the benefits of lower CapEx spend and how the corresponding increase in free cash flows has enhanced PAA’s balance sheet profile. During 2023 alone, PAA decreased its leverage ratio from 3.7x in 2022 to one of the lowest in the industry – i.e., 3.1x as of year-end 2023. PAA also made an adjustment to its capital allocation policy, lowering its long-term leverage ratio target range to 3.25x to 3.75x. As a result of this, the credit rating agencies recognized these positive movements and decided to strengthen PAA’s credit rating to mid BBB.

The reduction in leverage comes also with a benefit of interest expense savings, which boost the available cash flows for distributions. This coupled with strong EBITDA guidance for 2024 and favorable CapEx levels has made the current dividend coverage ratio of 190%.

In the most recent earnings call, Al Swanson – Executive Vice President & Chief Financial Officer, provided a nice color on what kind of dividends or distributions the unitholders can expect over the foreseeable future:

Well, I think, our current guidance for this year shows 190% coverage. So, we’ve got a bit to go our stated approach will be $0.15 a year until we hit the 160%. And then DCF growth will drive future increases there. So, we haven’t provided guidance for ‘25 or ‘26 yet. But yes, with this 19% or 20% increase we just did, we’re still at 190% coverage.

If we assume that the EBITDA remains constant and the aforementioned dividend hikes take place as planned (in $0.15 increments), the forward yield for 2026 lands at ~ 9%, which is very attractive.

However, I am rather confident that PAA will manage to gradually grow it EBITDA over time because of the following reasons:

- After making all of the dividends, CapEx and debt service related payments, PAA has still access to more than $500 million that could be deployed in incremental growth opportunities (primarily M&A).

- The improved credit rating and available cash flows for further debt reductions should keep the financing costs low, thus providing the necessary tailwinds for FCF that PAA could distribute to its shareholders.

This should warrant even a stronger base for PAA to surprise the investors to the upside by distributing even juicer dividends.

The bottom line

In my humble opinion, Plains All American is still a buy despite its massive alpha relative to the relevant index and its closest peers. On the one hand, investors have to understand that much of this share price run-up was linked to the recovery process from the abnormal hit during the pandemic years, which sent PAA way below its peers. Plus, the multiple (P/FCF) during the past 3-year period over which PAA registered outsized returns has not expanded at all. On the other hand, PAA’s core business is stronger than ever, as it has entered a structurally lower CapEx cycle and, on top of that, has already de-risked its balance sheet to historically low leverage levels. This in combination with attractive industry level outlook and huge surplus in the current dividend coverage creates a favorable ground for PAA to deliver on its objective to hike the dividend by $0.15 on an annual basis (at least until 2026).

For me, PAA looks like an attractively valued stock that complements nicely my income producing portfolio with stable and growing distributions over the foreseeable future. It is a buy.

Read the full article here