")

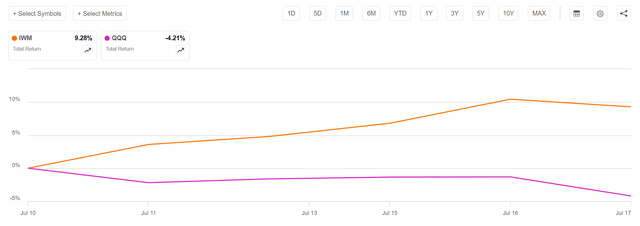

It has been a while since I last wrote about the Royce Micro Cap Trust (NYSE:RMT). Lately, we have seen a violent rotation in the equity markets. The small-cap-focused iShares Russell 2000 ETF (IWM) has rallied more than 9% since the benign CPI report on July 11th, while the mega-cap technology stock-heavy Invesco QQQ Trust ETF (QQQ) has fallen more than 4% (Figure 1).

Figure 1 – Violent rotation in the past week between small-caps and mega-caps (Seeking Alpha)

With this backdrop, I thought it would be helpful to revisit one of my favorite small-cap funds, the Royce Micro Cap Trust. We will examine how it has performed since my last article and whether there is any macro news investors should watch out for.

RMT Delivers Outstanding Short-Term Returns

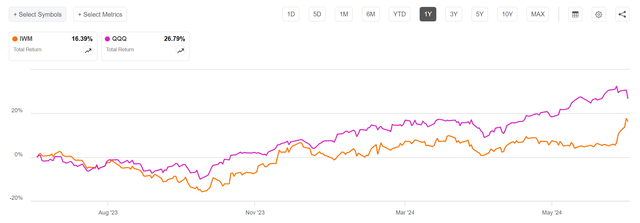

It is no exaggeration that since early 2023, investor attention appears to be singularly focused on artificial intelligence (“AI”) and the much-hyped mega-cap technology stocks like Nvidia (NVDA) and Microsoft (MSFT). This has led to underperformance by the broader indices like the equal-weighted S&P 500 and the Russell 2000. For example, even including the exceptional performance in the past week, the IWM still lags the QQQ ETF by 10% in the past year (Figure 2).

Figure 2 – IWM still lags QQQ by 10% over the past year (Seeking Alpha)

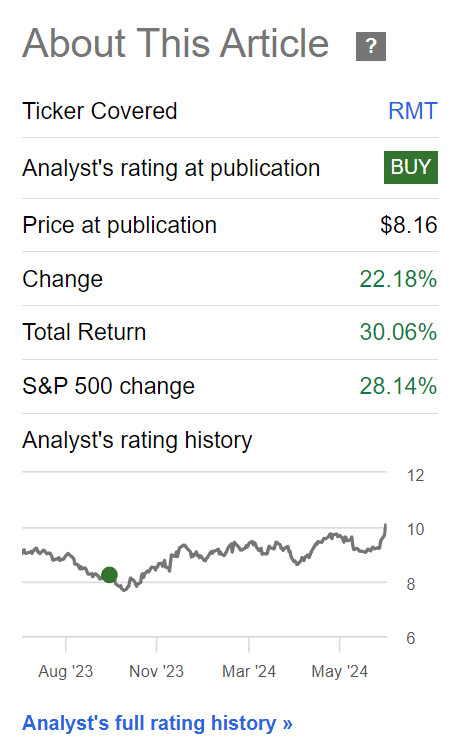

However, behind all the AI-hype and hoopla, fundamental-focused investors like Royce are having an excellent year. Since my article in October, the Royce Micro Cap Trust has delivered an outstanding 30.0% in total returns, beating the S&P 500 Index (Figure 3).

Figure 3 – RMT has outperformed the S&P 500 (Seeking Alpha)

So how does Royce do it?

Brief Fund Overview

Chuck Royce, the renowned small- and micro-cap investing expert and founder of Royce & Associates, describes his strategy as:

“Our task is to scour the large and diverse universe of micro-cap companies for businesses that look mispriced and underappreciated, with the caveat being that they must also have a discernible margin of safety. We are looking for stocks trading at a discount to our estimate of their worth as businesses.”

Basically, the RMT fund uses the time-tested “value investing” approach passed down by Benjamin Graham to look for underappreciated companies trading discounted to their intrinsic values.

There’s Still Alpha In Small-Caps

Unlike large-caps, where every company has dozens of analysts covering the stock (Apple has 43 Wall Street analysts covering it!), small-caps and micro-caps usually have little research coverage. It is up to the investor to do their due diligence and uncover security mispricings.

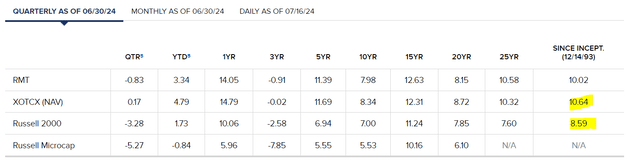

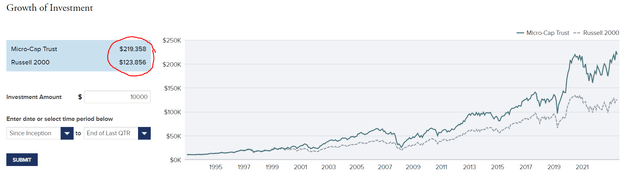

Over the years, Royce has had an exceptional track record of uncovering hidden gems and adding alpha. Since its inception in 1993, the Royce Micro Cap Trust has outperformed the Russell 2000 Index by an average of over 2.0% p.a., inclusive of the fund’s 1.76% expense ratio (Figure 4).

Figure 4 – RMT long-term outperformance (royceinvest.com)

While 2.0% a year may seem like a small number, when compounded over many years, the return difference can lead to a large difference in outcome (Figure 5).

Figure 5 – Compounding effect can lead to large differences in outcomes for investors (royceinvest.com)

Portfolio Holdings Update

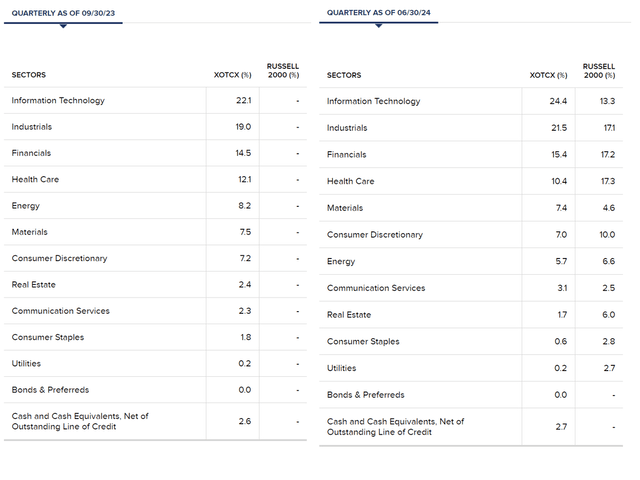

Since my last article in October, RMT’s portfolio allocations have remained relatively stable as the fund’s turnover is low at 30% p.a. (Figure 6). RMT’s largest sector weight remains Information Technology, increasing from 22.1% to 24.4%. Industrials also gained from 19.0% to 21.5%. Financials went from 14.5% to 15.4%. On the other hand, Energy stocks were materially cut from 8.2% to 5.7% while Health Care was trimmed from 12.1% to 10.4%.

Figure 6 – RMT sector allocation (royceinvest.com)

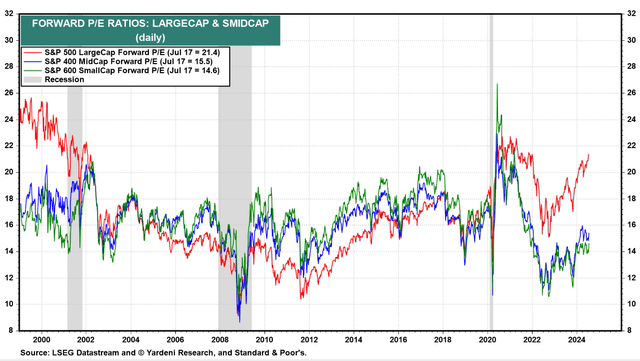

So far, while valuations on large-cap equities are fast approaching 2021 and 2000 bubble levels, valuations in small-caps remain ‘cheap’ and reasonable (Figure 7). Assuming the economy continues to grow, I expect small-cap stocks like those held by the RMT fund to outperform.

Figure 7 – Large-cap vs. small-cap valuations (yardeni.com)

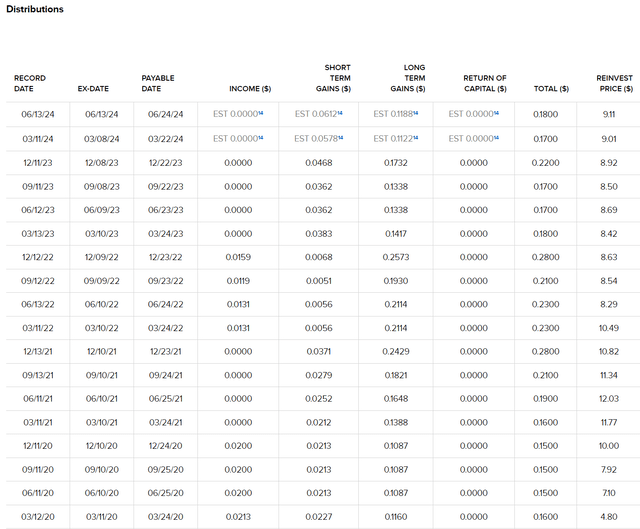

Distributions Trimmed But Remains Juicy

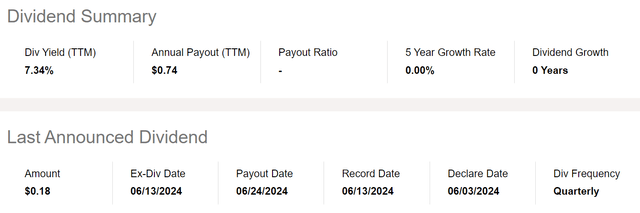

For income-oriented investors, the RMT fund may not be their preferred choice, as Royce follows a managed distribution policy (“MDP”), paying a quarterly distribution at an annual rate of 7% of the average of the prior four quarter-end net asset values (“NAV”).

In the trailing 12 months, this has worked out to a $0.74 / share distribution, a 7.5% decline from $0.80 / share mentioned in my prior article. The current distribution works out to a 7.3% yield on market price (Figure 8).

Figure 8 – RMT distributions have declined in the past year (Seeking Alpha)

While a decline in distributions is slightly disappointing, it is also not unexpected. The previous $0.80 distribution figure is based on a look back through 2022, when the fund was coming off strong 2021 returns (Figure 9). Going forward, if RMT’s investment returns continue to be strong, we should see a gradual increase in RMT’s distribution. There is also the prospect of a special distribution at year-end if investment performance has been strong.

Figure 9 – RMT distributions history (royceinvest.com)

The key point is that with an MDP, investors do not have to worry that RMT’s distribution will become unsustainable and deplete the fund’s NAV.

Dispersion Trade In Reverse

Returning to the lede of this article, I believe the short-term outperformance from small-cap stocks may not be fundamentally driven, as the magnitude and velocity of the moves suggest it is a big position unwinding from large hedge funds.

Coming into this year, one of the key macro trades I have been monitoring has been dispersion. Dispersion trading takes advantage of the difference between expectations of volatility priced into index options versus those on the individual components of the index.

Typically, a trader shorts index volatility (sell calls) and buys volatility (buy calls) on individual stocks like Nvidia or Microsoft. When the stock prices of Nvidia and Microsoft are rallying hard, other stocks must fall equally hard, such that index volatility remains low.

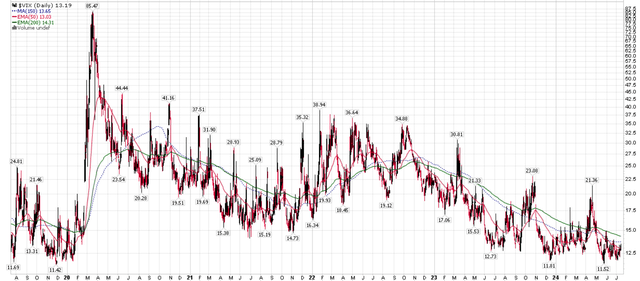

The rise of dispersion trading may be partly responsible for the collapse in index volatility in the past few quarters, with the S&P VIX Index (VIX) collapsing to multi-year lows, while the mega-cap stocks gap up to all-time highs (Figure 10).

Figure 10 – VIX has collapsed to multi-year lows (stockcharts.com)

My “spidey-senses” perked up in late 2023, when the CBOE launched the CBOE S&P 500 Dispersion Index, allowing institutional traders to track and trade dispersion. Brokers do not launch products from the goodness of their hearts; products are usually launched in response to strong customer demand and to lure in unsophisticated macro tourists.

However, when I saw podcasters start to discuss the complex dispersion trade in semi-professional discussions earlier in the year, I knew the dispersion trade’s days were numbered.

I believe we are currently seeing the unwind of these massive dispersion trades where small-caps and other S&P 500 components were used to fund long bets on the Magnificent 7.

The prospect of benign CPI inflation has once again raised hopes for rate cuts, which have boosted small-caps. As small-caps rise, the dispersion trade must go in reverse and cause sell-offs in the Magnificent 7 to keep index volatility contained.

My big fear is that as the moves become larger and larger, like the semiconductor stock crash on July 17th, an orderly unwind of dispersion trades can become disorderly and cause markets to flash crash. For the RMT fund, investors should watch out for rising market volatility and potential draw-downs as dispersion trades are unwound.

Conclusion

Although markets are focused on the “Magnificent 7” and the “AI investment theme,” the RMT fund has quietly delivered exceptional performance since my last article. This is a testament to the manager’s stock-picking prowess.

Looking forward, I am still constructive on RMT’s prospects, as valuations in small-cap equities remain quite reasonable. Assuming economic conditions do not deteriorate, I believe small-caps and the RMT should outperform.

However, recently, we have also seen a violent unwinding of dispersion trades that have kept market volatility low. If the moves continue, there is a possibility of a market crash as the unwinding becomes disorderly.

My advice for investors is to stay invested in the RMT, but keep an eye on the exit.

Read the full article here