")

Shares of Robert Half (NYSE:RHI) have been a poor performer over the past year, losing 6% even as the broader market has rallied significantly. Since recommending investors sell shares of RHI, the stock has lost 13% while the market has rallied 9%. Shares are also near my $72 price target. Given this magnitude of underperformance and the current share price, it is worth revisiting RHI to see if shares are now more attractive. The business continues to face negative momentum, and as such, I would not be a buyer of shares.

Seeking Alpha

Looking at its most recent financials reported on January 30th, RHI earned $0.83, which beat consensus by a penny even as revenue fell 13% to $1.5 billion. Earnings were down nearly 40% as the firm saw margins compress, given lower revenues. For the full year, it earned $3.88 from $6.03 in the prior year. In my view, the company also has a “quality” of earnings problem because in 2023, it made $112 million on interest income and income from investments in deferred compensation plans, adding over $0.80 of EPS.

Robert Half has an indisputably pristine balance sheet; it has no debt and $732 million of cash on hand, or about $7 a share. Thanks to Federal Reserve policy, RHI is able to earn 5+% on it cash, providing a nice source of income. Unless the Fed continues to raise rates though, this source of income is unlikely to grow, and should the Fed eventually cut rates, this income would fall. Because rates are widely seen as above their long-term average, many interest rate sensitive companies are trading at lower earnings multiples on the assumption they are “over-earning” their long-term average.

Many insurers trade below 12x earnings for instance. It is a good thing Robert Half has an excellent balance sheet, but interest income is not a source of earnings that merits a 20x multiple in my view. Rather, I prefer to look at RHI’s core business, value that, and simply add back the $7 per share that its cash position equates to.

Aside from the interest rate benefit, Robert Half’s core business of employee placement and temporary contract work is facing ongoing headwinds. As noted, revenue is down 13% from last year. This is fairly broad-based with US revenue down 16.7% from a year ago while its overseas business fell by 9.8%. Because of associated lost operating leverage, gross margin contracted 39.6%, down from 41.6% last year. Part of this decline is also coming from a slower conversion rate of turning contractors to full-time employees, as its customers have been hesitant to add headcount. In the face of these headwinds, Robert Half has managed to reduce SG&A spending by about 5.1% to $517 million, though this is still a smaller pace of decline than seen on revenue.

For the year, contract solutions revenue fell by 17% to $887 million; finance and accounting is nearly 75% of this unit. Permanent placements fell 22% while Protiviti was down a more modest 7% to $463 million. Now, given a near-record low unemployment rate, the fact that RHI is seeing weakness in its business may be surprising, but the macro environment is actually not that favorable.

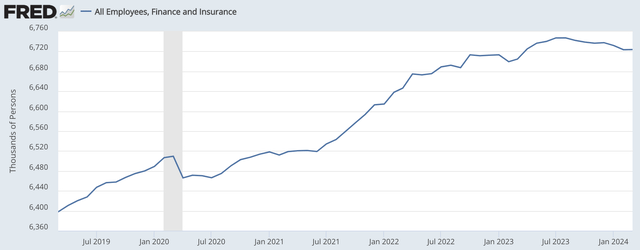

First, RHI is not exposed to variations in the entire labor market, so much as a specific subset of it. As noted, 75% of the company’s placement is tied to finance and accounting. What is occurring in manufacturing employment or construction employment, for instance, does not really matter. Interestingly, finance employment is actually 24,00 below its highs last summer, even as overall employment has continued to rise. Big banks have been reducing staff to manage costs, as they face an uncertain macroeconomic future. This is an ongoing headwind for the company.

St. Louis Federal Reserve

Management interestingly said the “tone” of client conversations had been improving, given “a more favorable interest rate policy” on the last earnings call. Accordingly, it expected greater hiring activity this year. Unfortunately, I am looking for a more cautious outlook alongside its next earnings report, which will be likely be in early May. At one point earlier this year, the markets were pricing in six rate cuts; that is now down to two. Quite simply the interest rate environment has turned much more unfavorable again. This ongoing volatility in the outlook is a reason why RHI’s customers have been unusually slow to convert contractors to employees as there is hesitance to commit to higher headcount.

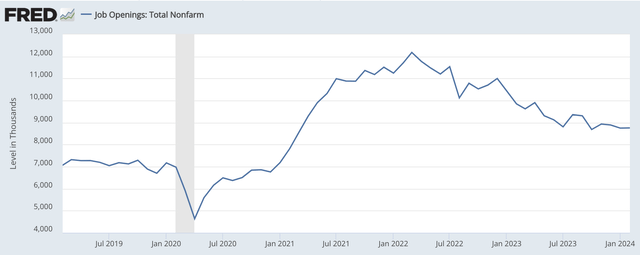

Indeed, in the macro data, I see no evidence of this improved tone leading to improved activity. Ultimately, Robert Half benefits from job market churn. As a placement service, it needs employers hiring. If unemployment is 3% but no employer is hiring or firing, simply retaining staff, that reduces the need for recruitment activity vs a 5% unemployment environment when there is significant job churn due to quits, layoffs, and hires. We appear to be in the first situation. As you can see below, job openings have fallen sharply over the past two years, and there is not yet evidence we are seeing a rebound. All else equal, fewer openings is likely to translate to lower hiring.

St. Louis Federal Reserve

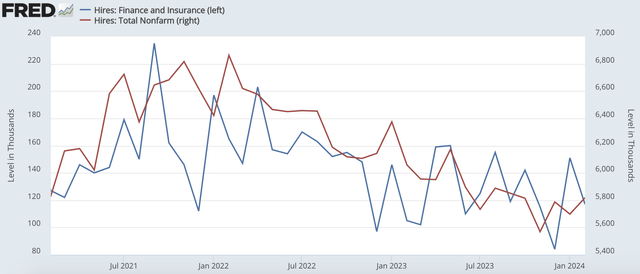

Indeed, that is what is playing out. Given its smaller sample size, finance and insurance hiring is even more volatile than total hiring. Still by either measure, hiring activity is running well below peaks seen in 2021-2022, which is likely to keep RH’s revenue environment fairly subdued.

St. Louis Federal Reserve

It is rare for employment activity to accelerate as the economic cycle ages; typically, it continues to slow, as fewer available workers are unemployed and employers get more fully staffed. Now if we do not have a recession (which is my base case), I expect hiring activity to continue to bounce around current levels, likely falling somewhat in the finance sector, but at a slowing pace from last year, in part due to easier comparisons.

Now over the medium term, I think there is also a risk investors should consider: AI. Many are predicting that as AI becomes more widely available, economic productivity should rise. Higher productivity of course means the same work can be done with fewer people. If this does play out, employment and hiring activity could slow further, particularly as many finance & accounting activities are very process-oriented, which could make AI adoption easier.

Personally, I believe forecasting the timing of major changes like AI is extremely difficult. Moreover, how quickly the technology is adopted is uncertain, and it can create employment opportunities elsewhere, and RHI could attempt to shift its recruitment and contract work to meet this demand. To be clear, I am not expecting mass unemployment due to AI. My concern is more that when hiring activity rebounds eventually; it could be slower than see in the past given ongoing productivity gains.

Frankly, in the optimistic case, we can see results remain around current levels assuming hiring activity is near its bottom, but in a recession, we could see further pressure. With the Fed holding rates higher for longer, I struggle to see a case for acceleration. Now with its strong cash position, it can continue to buy back shares, and subsequent to its quarterly release, Robert Half boosted its dividend by 10%, and shares now offer a 2.8% yield.

However, I see downside risk to sentiment when Q2 earnings are reported, likely in the next few weeks, given the less favorable macro. Excluding interest income, RH likely has $2.90-3.20 in earnings power assuming flattish revenue and margins near Q4 levels. Given its pristine balance sheet and strong free cash flow profile, I value this at ~20x or about $60, plus $7 in cash, for about a $67 fair value, lower than my $72 prior estimate as I had thought RHI could earn $3.60, when it seemed likely the Fed was poised to loosen policy more materially. With another 5+% of downside, I would continue to avoid RHI.

Read the full article here