")

I’ve been bullish on value over growth, but value as a style, outside of sector tilts, can be a bit subjective. Everyone has a different definition to some extent, and some ways of categorizing value stocks are better than others. One fund that approaches the value definition uniquely is the Invesco S&P 500® Pure Value ETF (NYSEARCA:RPV). The approach here scores companies are based on three primary factors: earning-to-price, book-value-to-price, and sales-to-price. The Pure Value in the name of the fund means it’s only focusing on those companies at the deepest end of these metrics.

Conceptually, I like this. It covers the fundamentals, and essentially positions where the metrics are cheapest. But the question is: Does it work? First, to set the stage, it’s important to note that value investing is inherently about buying cheap stocks. Benjamin Graham and Warren Buffett are well-known pioneers here, where momentum isn’t the cause of them making a stock purchase. If you are patient and don’t fall for FOMO (fear of missing out), value investing can be very rewarding. And especially pure value companies (one would think) as being the cheapest companies to purchase through the ETF wrapper of RPV.

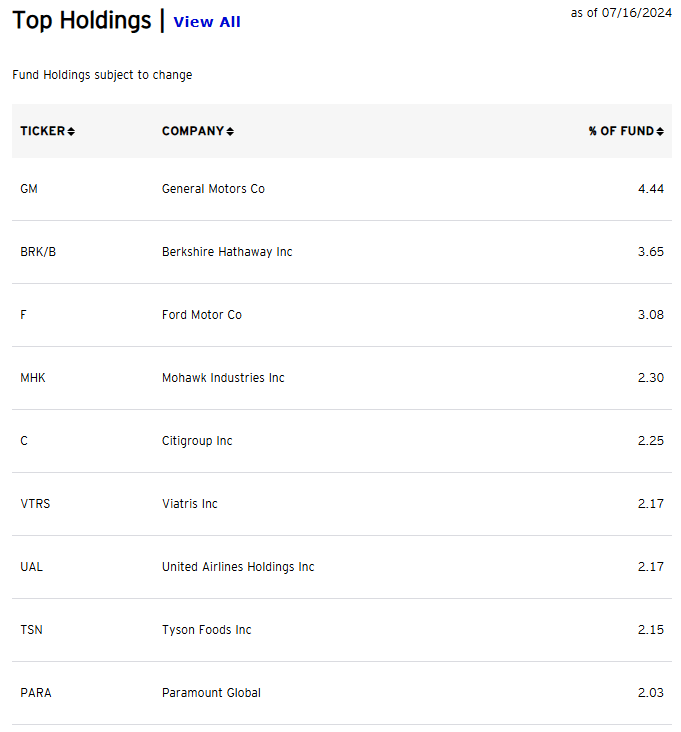

A Look At The Holdings

No position makes up more than 4.44% of the fund. The companies in the top 10 are for the most part all familiar ones, and perhaps can be considered “old economy” stocks.

invesco.com

What do some of these more old economies do? General Motors, of course, is the auto manufacturer. Berkshire Hathaway is Warren Buffett’s company. Ford Motor designs, manufactures, markets, and services a full line of vehicles. United Airlines is a major airline which operates an extensive domestic and international route network. And Citigroup is a multinational investment bank and financial services corporation.

None of these are particularly exciting companies, but that’s precisely why they are value. Most financial media doesn’t cover these companies anywhere near to the same extent as popular tech names. These are unloved companies, whose stocks fundamentally look undervalued. And given that the fund only holds 97 stocks, these should in theory be the most attractive names (from a valuation perspective, not a momentum one).

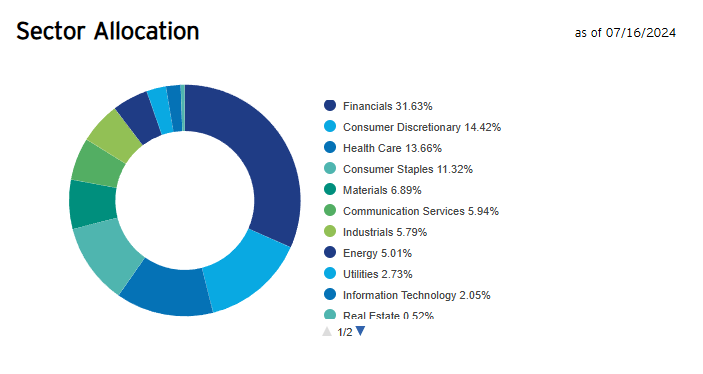

Sector Composition and Weightings

As is typically the case with value stocks, the majority of the fund is in the Financial sector.

invesco.com

Financials make up nearly a third of the fund, followed by Consumer Discretionary and Health Care. Tech? It’s at just 2.05%. Hardly a deep value sector. I actually do like Financials here and suspect that they can outperform, given how far removed we are from the regional banking crisis of last year.

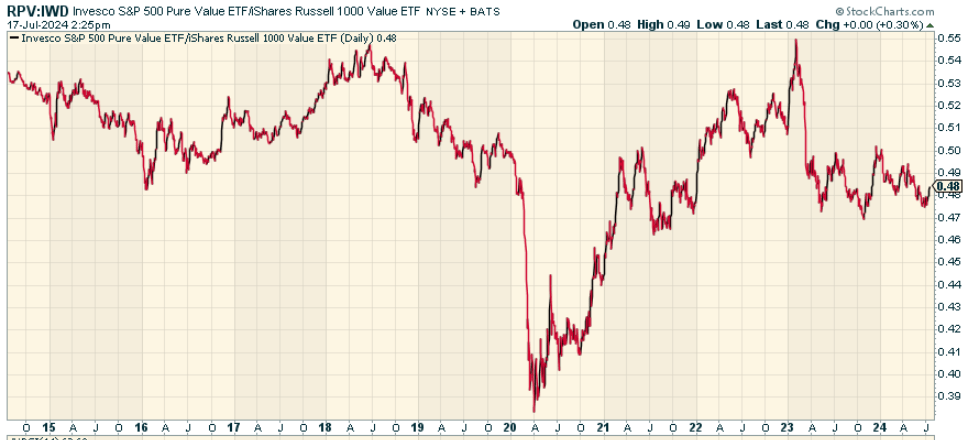

Peer Comparison

Since this is screening for the deep value names, it’s worth comparing the fund to the more passive iShares Russell 1000 Value ETF (IWD) which has a broader number of stocks categorized as value. When we look at a 10-year chart, the reality is pure value as defined by RPV has had roughly the same overall relative performance as the Russell value. Yes, there have been times of under and over-performance, but the two have stayed largely the same since late 2015.

stockcharts.com

Therein lies the question mark. Is it really worth creating a strategy around “pure value” when a less pure value definition yields roughly the same results over time?

Pros and Cons

The biggest positive here is the cycle. I believe we will see a big rotation out of growth and into value, which means largely out of Tech into everything else. The diversification of RPV, and methodology of determining what’s value and what’s not, should result in potential outperformance against the S&P 500 for years to come. I do appreciate the fund’s more rules-based approach to stock select as well in the way it weights and allocates to value stocks through its screening approach.

The downside? Maybe growth isn’t done, and perhaps these cheap stocks are cheap for a reason. There is a clear cyclical tilt in the sector allocations here, with Financials and Consumer Discretionary making up the biggest weightings. Any kind of recession, no matter how cheap these stocks are now, would bring these positions lower and punish investor demand. The value trap potential is very real, and can’t be ignored.

Conclusion

The Invesco S&P 500® Pure Value ETF seeks to provide exposure to economically sensitive, fundamentally sound, undervalued stocks representing the S&P 500 universe. With a robust multifactor valuation model at its core, RPV embraces a systematic and rules-based implementation of the value strategy. I think it’s an interesting and good fund, though I don’t feel compelled to choose this over a broader value portfolio like IWD and others. Good fund, though, regardless, for what it’s trying to do.

Read the full article here