")

SalMar (OTCPK:SALRY)(OTCPK:SALRF) saw the improvements in the Scottish businesses that we expected in our last coverage as a turnaround from last year’s more troubled volumes. However, Northern Norway and Iceland instead experienced biological issues that hit current volumes and worsened the incoming harvest to weigh on hoped for results. Since the close of the quarter, spot prices started on their way down, which may start to impact the segments with lower contract share, mostly in Norway, where profits are more concentrated. Nonetheless, some increase in operating profits are expected. However, we don’t expect much YoY net profit performance due to the new tax, higher tax levels on salmon companies. More major net profit improvements should only be expected onward from next year, if even then. In general, fairly valued at PEs likely above 20x.

Latest Earnings

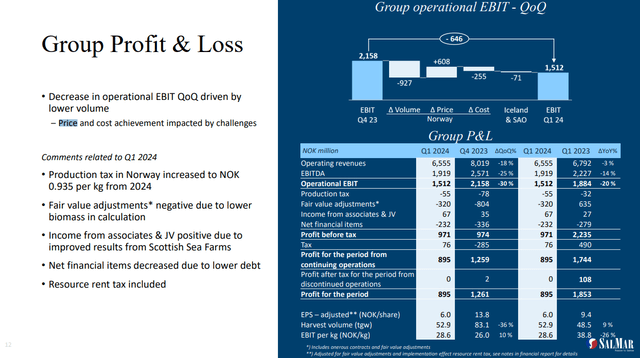

The situation in the latest Q1 earnings has been that biological issues have forced some early harvests, which raises the cost per kilo, has hampered tonnage and reduced margins. Salmon prices were good at this point on the spot market, though, which had an offsetting effect.

Group Level P/L (Q1 Pres)

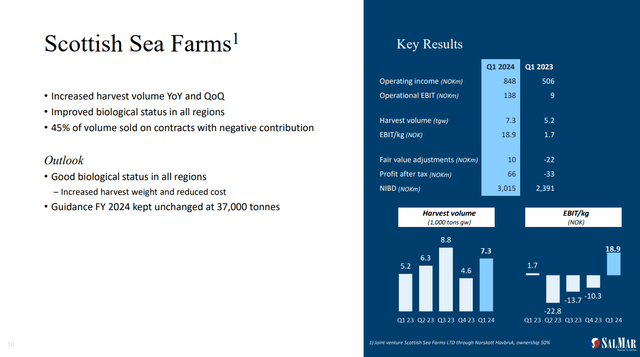

Central Norway and Scotland did well. Scotland was weighed down last year, but they have started to get ahead of environmental challenges impacting the fish. Volumes were therefore up significantly, although the higher contract share mitigated the help from stronger spot prices as of the quarter’s close. Going from a negative to a nicely positive contributor has been one of the bigger helps.

Scottish Farms (Q1 Pres)

Northern Norway is one of the geographies that really struggled on account of attacks from jellyfish, which forced some earlier harvests than the company would have liked. Cost per kilo will remain elevated next quarter as well, according to the company. Volume guidance is still on, but the earlier harvests than hoped are a bit unfortunate, and realistically this segment will be behind internal expectations of profits by the end of the year. It’s a big segment, almost as big as central Norway, which are the two principally profitable segments where the other ones flirt with negative margins as soon as any environmental impact hits.

Iceland was another problem area, again due to environmental issues with lice. Some non-recurring incidents at sea also had an impact on profits, but primarily issues with lice inflated the cost base due to disposals and inefficient harvests. This segment is also not terribly robust and profitable, but the company’s organic initiatives are looking to increase tonnage by around 30% following a possible issue of a license to SalMar, details forthcoming.

Bottom Line

In general, harvest volumes are still on target for the year, although they would have hoped to post growth and start getting ahead of the new taxes, and the offshore salmon project is also seeing some incremental profit improvements, with the company gaining confidence in this new mode of aquaculture, despite effects from string jellyfish there as well. Overall costs should start to decline in the second half of the year, but volume will likely be limited in growth. Salmon prices are also on the way down again, which will start to weigh on the Norwegian business, which is more profitable and employs less contract share. Contract share is also higher now than they expect it to be towards the end of the year, which has limited the benefits from decent salmon prices these last couple of quarters. Pricing benefits should become mitigated.

In our previous coverage, we explained how we might arrive at an EAT figure. We think that even before tax, profits will likely take a small hit this year of a couple of percent. On top of the significantly higher tax burden, SalMar is still looking at a 25x PE. It’s hard to draw a close peer within aquaculture because the business mixes differ, including by geography, which matters a lot, but suffice it to say that a 25x PE is not a low multiple, although we think it is fair in the context of the high ROIC that SalMar generates.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here