")

Investment Thesis

The Schwab U.S. Small-Cap ETF (NYSEARCA:SCHA) ranks well in categories like assets under management, expenses, liquidity, and diversification. However, SCHA’s disappointing quality led to my “sell” rating in May 2023. In the year since, SCHA has delivered a total return of 20.02%, lagging behind higher quality peers like the Vanguard Small Cap ETF (VB) and more concentrated Invesco S&P SmallCap Momentum ETF (XSMO) by 1.86% and 17.38%, respectively. SCHA’s one-year returns ranked #25/49 in the small-cap blend category.

Portfolio Visualizer

These results aren’t bad by any stretch. However, while I firmly believe better choices are available, I’ve decided to upgrade SCHA because of its above-average rankings on growth and sentiment. I also want to express how adding small-cap stocks to your portfolio at this stage is wise, as recent earnings results for many holdings were well above expectations. I hope you enjoy the analysis, and as always, I look forward to your questions afterward.

SCHA Overview

Strategy and Performance

SCHA tracks the Dow Jones U.S. Small-Cap Total Stock Market Index and has an outstanding 0.04% expense ratio. That’s only one basis point more than the SPDR S&P 600 Small Cap ETF (SPSM) and 0.105% less than the 0.145% category average. But over the last three years, we’ve seen higher-fee funds do much better. XSMO has led the category with a 15.66% total return from May 2021 to April 2024 despite its high 0.39% expense ratio. Meanwhile, SCHA’s -6.28% total return ranks a disappointing #43/49 in the small-cap blend category. There isn’t necessarily an inverse correlation between fees and returns for small caps, but rather, there is no correlation at all. Therefore, we need to put SCHA’s low expense ratio out of our minds and focus the analysis on the other more important features, like its strategy and fundamentals.

The Index divides the U.S. Total Stock Market into three size segments: small-cap, mid-cap, and large-cap. The small-cap segment includes those ranked 751-2500 by total market capitalization (i.e., not float-adjusted), and then the Index weights constituents by their float-adjusted market capitalizations. Common stocks and REITs are eligible, though BDCs, LPs, ADRs, and other alternative share types are not. The Index reconstitutes annually in September and rebalances quarterly.

Overall, the strategy is pretty simple. Investors gain access to a broad group of 1,750 small-cap companies weighted by size. As a small-cap investor, your decisions will revolve mainly around the number of holdings you want exposure to and whether a company’s size is an appropriate weighting tool. My view is that the number of holdings is excessive, and unlike large-cap stocks, size is not always correlated with quality.

Diversification Analysis

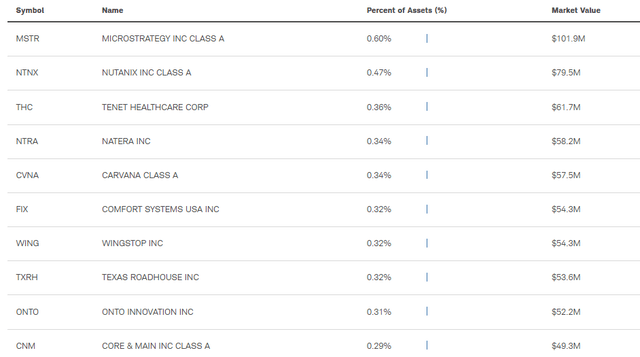

SCHA’s top ten holdings are below, totaling 3.67% of the portfolio. This table won’t help us much, as there are just too many holdings to sort through, and this list does not represent the portfolio well. For example, MicroStrategy (MSTR) and Nutanix (NTNX) are SCHA’s top two holdings, representing about 30% of the top ten. However, their GICS sub-industry, Application Software, represents only 5% of the portfolio.

Schwab

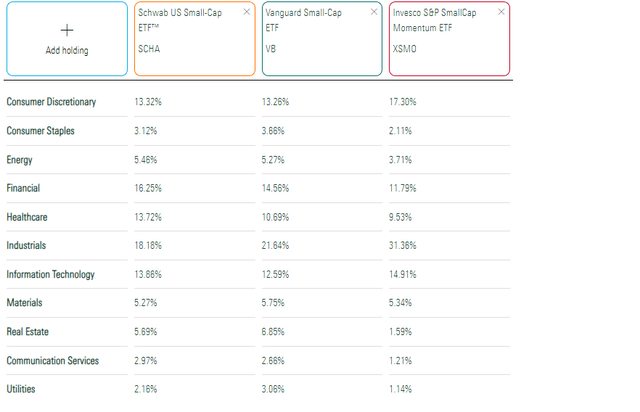

SCHA’s sector exposures, alongside VB and XSMO, are listed next. Notice how no sector in SCHA comprises more than 20% of the fund, a feat slightly missed by VB. In contrast, XSMO has 31.36% allocated to Industrials. As a momentum-based ETF, assets flow to whatever holdings performed best, resulting in relatively high portfolio turnover. You won’t get that with SCHA, as its annual report lists portfolio turnover rates between 9% and 15% over the last five years.

Morningstar

Finally, I’ve ranked all small-cap ETFs on diversification at the sub-industry level, which is a compromise between company- and sector-level concentration analysis. SCHA, VB, and XSMO rank #10/49, #2/49, and #48/49, respectively, so the less active ETFs have the diversification advantage. Intuitively, a substantially different portfolio is required if you want to beat the market, but this approach often comes with risk, so I still view diversification positively.

SCHA Factor Analysis

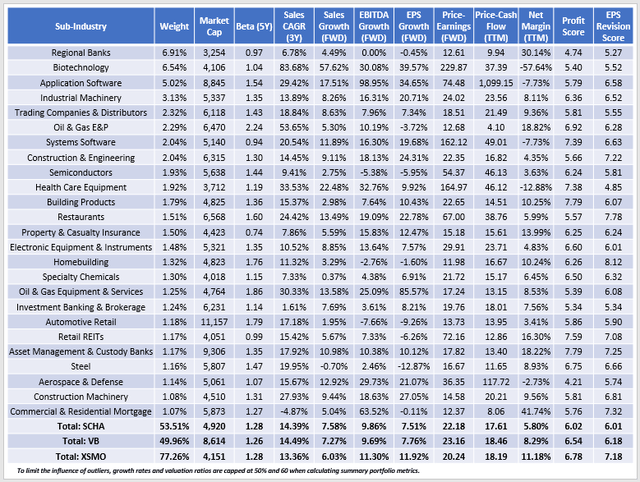

The following table highlights selected fundamental metrics for SCHA’s top 25 sub-industries, totaling 53.51% of the portfolio. VB’s exposure to its top 25 is slightly less at 49.96%, while XSMO is the most concentrated at 77.26%, mainly due to the fund holding only 115 stocks.

The Sunday Investor

I want to use this table to discuss how SCHA ranks on six key fundamental metrics: risk, value, growth, quality, and sentiment. This focus moves us away from metrics that haven’t provided much value in recent years, like expenses and assets under management.

Risk: #41/49

SCHA’s 1.28 five-year beta is the 41st highest in the small-cap blend category. However, it’s only slightly above the 1.25 median figure, reminding investors that higher volatility is normal for this segment. Therefore, I wouldn’t let this rating deter you too much, as the only way to avoid it is by holding low-volatility funds like the ones below:

- Invesco S&P SmallCap Low Volatility ETF (XSLV)

- SPDR SSGA US Small Cap Low Volatility ETF (SMLV)

- iShares MSCI Minimum Volatility USA Small Cap ETF (SMMV)

Value: #34/49

SCHA trades at 22.18x forward earnings and 17.61x trailing cash flow and has a 4.48/10 Value Score, which I derived using individual Seeking Alpha Factor Grades. This score ranks #34/49, indicating that SCHA is slightly more expensive than its peers. The table shows it’s cheaper than VB but two points more costly than XSMO. One concerning sub-industry is Biotechnology, which comprises 6.54% of SCHA. My calculation method limits the impact of its 229.87x forward P/E ratio. However, it’s worth noting that most alternatively weighted peers have limited allocation to these stocks, several of which have limited sales.

Growth: #9/49

In addition to solid diversification, growth is one of SCHA’s best features, evidenced by a 5.80/10 Growth Score that ranks #9 in its category. Fortunately, high growth rates aren’t limited to only a handful of sub-industries, but analysts are particularly bullish about Application Software and Systems Software stocks. SCHA’s 106 holdings in these sub-industries comprise 7.06% and have grown sales by an annualized 23.70% over the last three years. High growth potential is a key reason investors should consider small caps, but it’s also worth pointing out that VB and XSMO are strong. In particular, XSMO features an estimated earnings per share growth rate 4.41% better than SCHA, and has an overall growth score that ranks #3.

Quality: #31/49

SCHA’s 6.02/10 Profit Score ranks #31/49, which is below average and the main reason for my prior “sell” rating. There are many ways to measure profitability, but I’ve included each sub-industry’s weighted average net margin figures as evidence that there is a lot of “junk” in these Indexes that cover the entire small-cap segment. I’ve highlighted the Biotechnology sub-industry, which has minimal exposure in quality-focused funds like the Invesco S&P SmallCap Quality ETF (XSHQ). However, Application Software and Systems Software stocks also have negative net margins, making the trade-off clear: they’re speculative plays with excellent growth potential but unattractive value and quality features.

Sentiment: #13/49

I use Seeking Alpha EPS Revision Grades to measure sentiment, as it provides an objective way to identify which stocks Wall Street is optimistic about. On a ten-point scale, SCHA’s weighted average score is 6.01/10, or #13/49 in its category. While above average, it’s a bit behind VB and XSMO, whose scores rank #5/49 and #2/49, respectively.

Often, positive earnings revisions result from solid quarterly results, and this was certainly the case last quarter. SCHA, VB, and XSMO had last quarter earnings surprises of 12.23%, 11.17%, and 14.75%, respectively. For reference, earnings surprises for the Schwab U.S. Mid-Cap ETF (SCHM) and the Schwab U.S. Large-Cap ETF (SCHX) were 10.45% and 7.25%, so the smaller stocks have impressed the most recently. For this reason, now might be a good time to add this segment to your portfolio.

Investment Recommendation

SCHA does a lot of basic things well. It has a low 0.04% expense ratio, is well-diversified, and is one of the most liquid small-cap ETFs on the market. My fundamental analysis revealed it’s also strong on growth and sentiment, and given how small-cap stocks seem to have an earnings surprise advantage over large-cap stocks, I’ve decided to upgrade my rating on SCHA to a “hold.” However, I don’t think it’s the best choice due to weaknesses in value and quality. More concentrated ETFs like XMSO and XMHQ have better fundamentals, and even VB, another low-cost and well-diversified fund, has the advantage on most of the fundamental metrics I evaluated today. Thank you for reading, and I look forward to your comments below.

Read the full article here