")

Note:

I have covered SEACOR Marine Holdings Inc. or “SEACOR Marine”(NYSE:SMHI) previously, so investors should view this as an update to my earlier articles on the company.

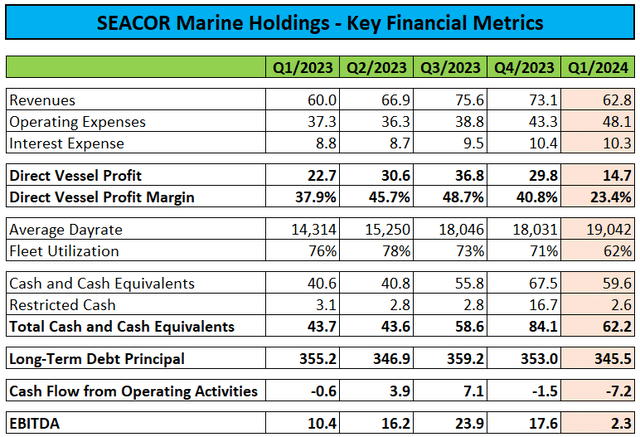

Two weeks ago, leading offshore support vessel provider SEACOR Marine Holdings reported disappointing first quarter results, with revenues and profitability falling well short of expectations:

Press Releases / Regulatory Filings

While the company’s average dayrate of $19,042 represented another multi-year high, fleet utilization of just 62% dropped to its lowest levels in recent years.

In the press release, management attributed the decrease to seasonality as well as the company’s decision to conduct scheduled maintenance and reposition vessels during the winter months:

The first quarter results reflect both continued improvement in dayrates as well as lower seasonal utilization. We have been deliberate with our plans to conduct scheduled maintenance and reposition vessels during the winter months. These efforts incurred higher operating expenses and lowered utilization, resulting in a decline of our DVP metric as we expense drydocking and major repairs as incurred. We continue to achieve improved terms and pricing as vessels roll off contracts, and we expect significantly improved utilization as we complete vessel repositioning and enter new contracts.

However, the domestic U.S. market was particularly weak, with revenues down by almost 60% sequentially due to seasonality as well as delays in decommissioning activities and offshore wind projects. As a result, direct vessel profit, the company’s equivalent to gross margin, turned negative for the U.S. segment.

SEACOR Marine recorded negative free cash flow of $10.6 million for the quarter and utilized another $11.4 million for debt repayments and tax withholdings on restricted stock vesting.

The company ended the quarter with $59.6 million in unrestricted cash and cash equivalents, down $17.9 million quarter-over-quarter, while debt obligations amounted to $345.5 million.

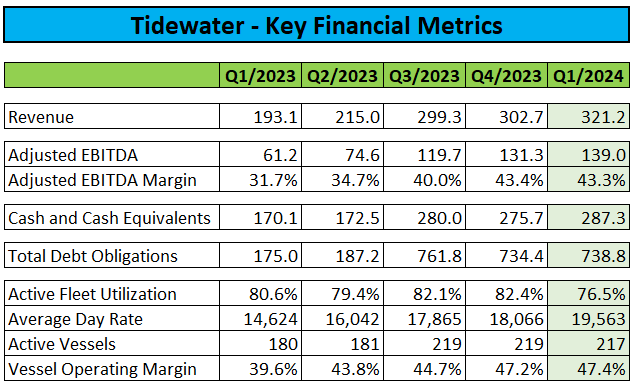

SEACOR Marine’s disappointing Q1 results were in sharp contrast to market leader Tidewater’s (TDW) rock solid first quarter report:

Company Press Releases

Please note that Tidewater achieved sequentially higher revenues despite seasonally lower utilization, with profitability reaching new multi-year highs.

That said, SEACOR Marine expenses all maintenance and drydocking costs rather than capitalizing parts of them on the balance sheet, which understates the company’s margins and profitability relative to Tidewater.

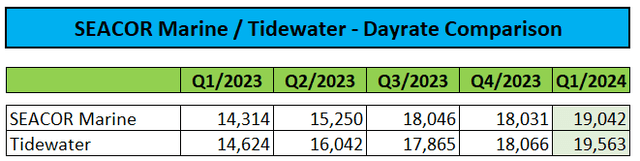

At least the year-over-year dayrate trajectory was similar, with both Tidewater and SEACOR Marine showing an encouraging 33% increase:

Press Releases

As outlined by management on the conference call, Tidewater does not expect a lasting impact from Saudi Aramco’s recent decision to suspend the contracts of 22 jack-up rigs:

In the Middle East, with the recent news in Saudi Arabia, we may see some short-term demand slowdown specifically related to work in the Kingdom.

However, we continue to see significant demand requirements from other countries in the region, as well as from the contractors supporting projects already ongoing in the kingdom that we expect will more than offset any near-term slowdown that we may experience from a rig count reduction in Saudi Arabia.

That said, given SEACOR Marine’s material exposure to Saudi Aramco (ARMCO) which contributed 15% of total revenues last year, it seems prudent to model some negative near-term impact.

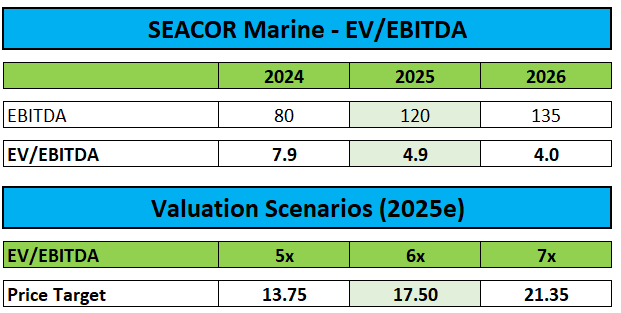

Considering the slow start to the year and some potential near-term weakness in Saudi Arabia, I have reduced my expectations for 2024. In addition, I have taken a more conservative approach towards 2025 and 2026:

Author’s Estimates

Based on an assigned multiple of 6x my estimated 2025 EV/EBITDA, I am reducing my price target from $20 to $17.50 while reiterating my “Buy” rating.

Bottom Line

SEACOR Marine Holdings reported disappointing Q1/2024 results, with utilization dropping to new multi-year lows and sizeable cash outflows.

While the company’s average dayrate continued to increase, the slow start to the year, in combination with some anticipated short-term pressures in Saudi Arabia, have caused me to revise my estimates.

Consequently, I am reducing my price target from $20 to $17.50 while reiterating my “Buy” rating.

Read the full article here