")

Sensient Technologies Corporation (NYSE:SXT) is a specialty ingredients company which primarily makes flavors and extracts. It produces dehydrated goods such as onion flakes, paprika, celery, and so on for food products along with synthetic flavors, coloring agents, and so on. In addition to the food industry, Sensient serves beverage, consumer wellness, and cosmetics firms.

In theory, this might sound like a great business. Companies like McCormick & Company, Incorporated (MKC) earn excellent profit margins selling spices and flavorings. However, Sensient has a much different business than a consumer-packaged goods company. Because Sensient is primarily selling to other businesses, rather than end consumers, it doesn’t get the sort of margin lift typically associated with branded food and beverage goods.

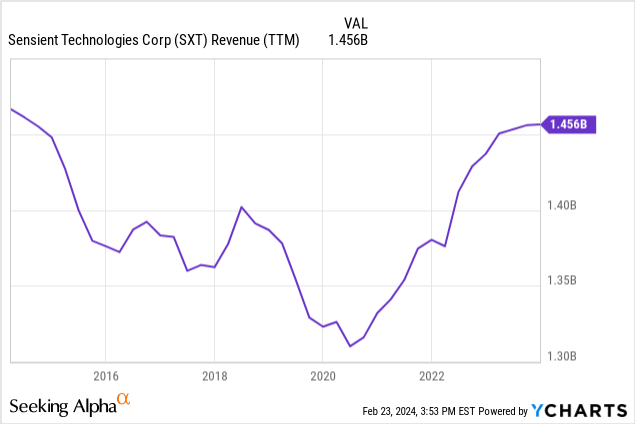

It also appears that the basic ingredients space is quite competitive. To that point, Sensient has not managed to grow revenues over the past decade:

Sensient’s revenues slumped between 2014 and 2020. And while they have recovered a bit now, they are still below the prior peak, to say nothing of where they would have to be to keep up with inflation over the years.

Last February, I covered Sensient shares and assigned a Hold rating, saying that the company was not cheap enough given its lack of growth. But with a year’s worth of developments, has my outlook changed?

A Year of Underwhelming Earnings

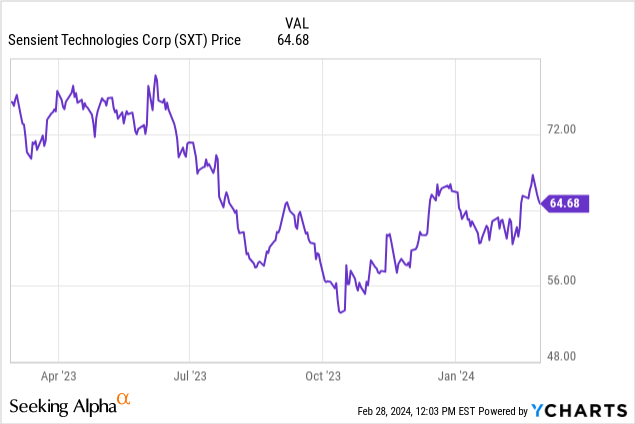

A few months ago, I was starting to think that we could be approaching an entry point for Sensient shares. The company’s shares had dropped quite substantially, moving from the $70s to the $50s:

Over the summer, Sensient shares dropped about 25% peak-to-trough, which is quite a big move for a low-beta defensive company such as this one. Since October, however, SXT stock has recovered a fair bit of its losses. If the company’s earnings had turned the corner, that’d be one thing. However, Sensient’s earnings have continued to worsen, though management is anticipating improvements in 2024.

Sensient released its Q4 2023 earnings report on February 8th. The company’s 51 cents of non-GAAP earnings missed expectations significantly and fell from the 64 cents that it earned in the same quarter of 2022. Revenues of $349 million were flat year-over-year and also missed expectations.

Sensient’s EBITDA margin slipped for the quarter, falling to 8.5% on account of lower sales volumes.

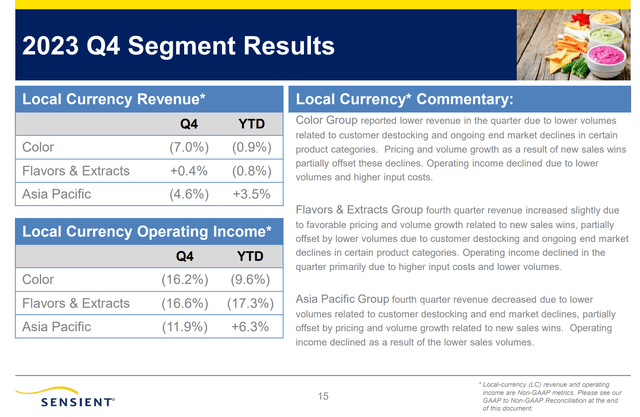

Here’s the company’s Q4 segments results slide — this is not a pretty picture:

Sensient operating results (Corporate Presentation)

It’d be one thing if the stock sold off to 52-week-lows on these results and there was a dip-buying opportunity. But it’s hard to get excited about the company with shares up significantly on these thoroughly mediocre operating results.

Management is making its best efforts to turn things around. It is implementing a portfolio optimization plan in an attempt to lower costs and improve its profit margins. While that is likely the right move in the longer term, it comes at an upfront cost. On a GAAP reported basis, Sensient outright lost money this quarter as it takes one-off expenses to implement its portfolio optimization plan.

Piled on top of Sensient’s other underwhelming 2023 quarterly reports, there was little reason for optimism here, and SXT stock initially sold off more than 5% following the release of that earnings report earlier in February. Since then, however, shares have rallied back to the mid-$60s.

What’s The Long-Term Earnings Power?

Let’s put the string of weak 2023 quarterly results aside for a minute. What’s the bigger picture for Sensient?

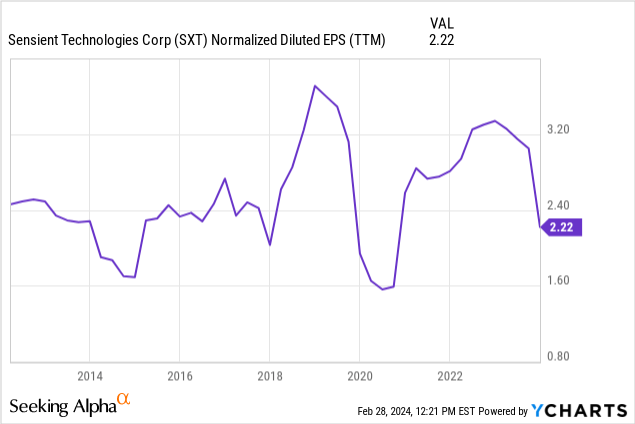

Given the firm’s lack of revenue growth, not surprisingly, earnings per share growth has been hard to come by as well:

Sensient was generating about $2.50 per share in normalized earnings per share throughout most of the 2010s. This popped up above $3.00 in 2019 and in 2022. However, with 2023’s sour results, earnings per share fell back to Sensient’s longer-term average in the low-to-mid $2s. Clearly, Sensient is not a cheap stock based on 2023’s results.

However, we should probably put 2023 aside. There were special circumstances last year, and the company is restructuring and optimizing its operations. I don’t believe the firm’s core earnings power is as low as what it generated in 2023. Analysts are forecasting about $3.00 per share in earnings for 2024, which seems about right based on the company’s projected revenues and historical profit margins.

Given how lousy 2023 was for Sensient, I am giving the benefit of the doubt to assume that the company will get back to $3 per share in earnings. However, that is in line with management’s guidance, which is upbeat. Here’s CEO Paul Manning from the latest conference call:

“As we begin 2024, we are already seeing an improvement in customer order patterns. We expect sequential improvement in our volumes throughout 2024, and I expect a much-improved financial picture, including solid sales, volume growth, local currency, revenue growth, and local currency-adjusted operating profit growth.”

That’s quite a positive statement and probably explains why shares have bounced despite such a tough Q4 2023 earnings report. That said, even if we assume 2024 is much improved and Sensient puts up the projected $3.00 of earnings per share this year, would SXT stock be a buy? I’m not convinced.

Sensient’s Bottom Line

Sensient Technologies Corporation has not shown consistent meaningful earnings growth over the past decade. EPS was up slightly, at least until last year. But that was largely a factor of the firm’s share buyback plus a bit of margin improvement. With no growth in top line revenue, it is hard to generate much consistent increase in earnings per share.

The company should return to around $3.00 of earnings per share this year, and analysts forecast modest growth from that level going forward. Unless and until Sensient can deliver sales growth, though, it’s hard to see EPS growth much beyond 2-3% per year.

At today’s price, if we figure 2% annualized EPS growth and the 2.5% dividend yield and that gets to mid-single digits annualized return assuming a stable P/E ratio. Given Sensient’s underwhelming past results, however, it’s not hard to imagine a scenario where there is no EPS growth from the starting $3.00 base, and a P/E ratio that trails off into the high teens. In that case, SXT stock would deliver essentially no total return over the next five years. And for a bull case to play out, we’d need a lot more organic growth than the company has shown over the past decade.

With the stock in the mid-$50s, you can pencil out acceptable total returns even in a low-growth scenario. From this price, though, I just don’t see the appeal. This is the sort of business that I want to like in theory, but in practice, the operating results simply aren’t compelling enough.

That’s especially true as so many consumer staples stocks have sold off sharply over the past 24 months. I am keeping Sensient Technologies Corporation on my watch list, but the company really needs to show more operating momentum in earnings to reset the narrative here.

Read the full article here