")

Investment Thesis

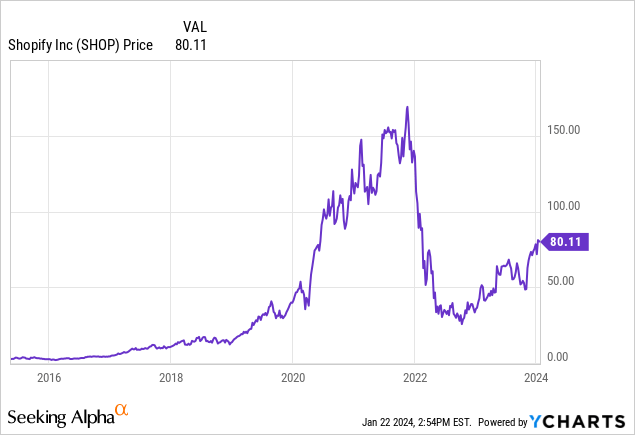

Shopify (NYSE:SHOP), a Canadian e-commerce giant, is on a run the last few quarters, with new record highs in operating income while still posting very high double-digit revenue growth in excess of 25% YoY. Since our Buy rating at $29.75, Shopify is up 170.89% in less than 15 months, making it one of our most successful investment ideas of the past two years.

We also pointed out in our first article that we have worked with Shopify and really like their product, which is why we take another look at whether Shopify is still a good investment idea at current prices after the big run-up. We examine both headwinds and tailwinds that affect our thesis and provide an updated valuation based on our updated assumptions.

A Return To Efficiency

There has been a strong trend among public tech companies with 2023 turning out to be the year of efficiency, largely started by Meta (META) in the first quarter of last year. Shopify was no stranger to this and has admitted that it hired too many people during the 2020 and 2021 e-commerce boom, and had laid off 20% of its staff in March last year and even 10% the previous July.

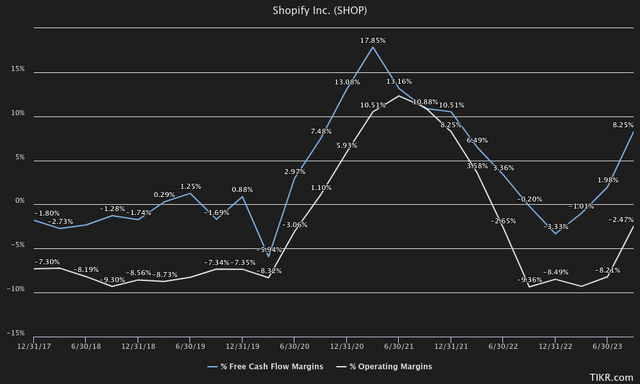

Shopify also made this focus on efficiency clear in Q2 of last year by announcing the sale of Shopify Logistics & Deliverr to Flexport in exchange for a 13% stake in the company. Although it seems like a write-off after last year’s $2BN purchase of Deliverr, Shopify CEO Tobias Lütke may be right in shifting the focus to the more important AI revolution compared to the logistics side of the business. If we look at Shopify’s operating margins of -2.47% and free cash flow margins of 8.25%, we see that they have improved significantly on a trailing-12 month basis after crashing in 2022 following the boom periods of the two years prior.

TIKR Terminal

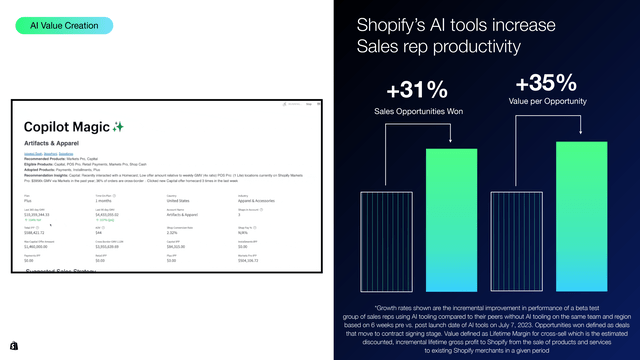

And while these margins are heading nicely north, we want to highlight a few factors as to why we think there is a bit more room for upside. One of the main factors we see at play is artificial intelligence, where Shopify seems to be taking a different path than other software companies such as Microsoft (MSFT) and Google (GOOG). Shopify seems to be going down the integration route rather than developing very capital-intensive and experimental large language models.

What we think is that many people are actually overlooking the fact that Shopify could be one of the key players to take advantage of the AI boom if we look at their core product. First, if you look at Shopify’s LinkedIn page, it becomes pretty clear that a huge portion of their workforce is assigned to software engineering and customer service/sales. All of these areas will benefit tremendously from AI by both increasing productivity and replacing repetitive tasks. For example, their coding workforce and human capital efficiency could get a huge boost as AI improves the efficiency of programmers.

From a customer support perspective, Shopify also benefits greatly from AI both internally and externally. Shopify can integrate AI not only through communication with their own customers, but has also built apps on top of their platform that Shopify customers can integrate to communicate more effectively with their own store’s customers. Even in other areas of marketing and content creation, Shopify can continue to experience tailwinds to build on top of by implementing AI and increasing the number of services offered, increasing customer loyalty and thus hypothetically increasing revenue.

Shopify Investor Day

Suboptimal Conditions

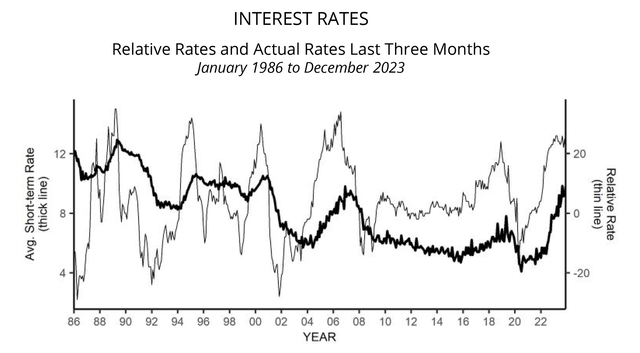

Setting aside the tailwinds from the factors mentioned earlier, in the grand scheme of things, we see quite a few headwinds in terms of macroeconomics that could certainly play a big role in Shopify. First, looking at statistics from the National Federation of Independent Business (NFIB), we see that optimism for small businesses is still at an all-time low.

While the S&P 500, or more specifically the magnificent 7, are trending upward, this does not seem to be the case at all for small businesses. In the survey, small businesses continue to report problems ranging from labor quality/supply to persistent inflationary pressures. On top of that, interest rates have skyrocketed over the past three years and are currently relatively close to their highest level ever. Small businesses currently pay an average of 9.8% on short-term loans, the highest interest rate in more than 20 years.

NFIB

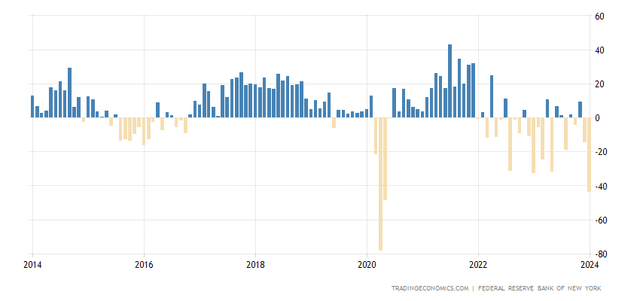

Speaking of interest rates, another major headwind and predictor of an impending recession is the 2-year 10-year interest rate spread, which is slowly reversing. In previous recessions, after the yield curve has been inverted for as long as it is now, the economy has always experienced recession after un-inversion. The Empire State Manufacturing Survey reflects business conditions and the possibility of a recession quite well, as it is now down to -43.7% in January, or its lowest since May 2020. In a recession scenario, Shopify, which focuses primarily on small and medium-sized businesses, could face some headwinds in the coming quarters.

Tradingeconomics.com

Growth At A Reasonable Price

The biggest problem we are currently facing in finding value in Shopify’s stock is not related to the core business which we like, but rather to the risk of overpaying for the stock. When the stock was trading at $29, and we were using valuation models, even with very cautious numbers we felt that the stock was too cheap and trading below fair value.

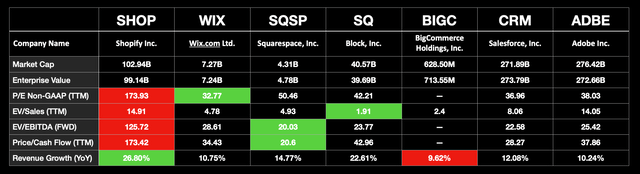

This time, we also find it very difficult to justify Shopify’s valuation on a relative basis. If we were to take Shopify’s record operating income last quarter of $224M and annualize it to $896M, the stock would still be trading at more than 115x last quarter’s annualized operating income at a valuation of $103.2BN. Comparing this to competitors such as Wix (WIX), Squarespace (SQSP), Block (SQ) and BigCommerce (BIGC), Shopify sticks out like a sore thumb based on valuation. Shopify is most expensive based on P/S, EV/EBITDA and P/FCF.

Seeking Alpha Data (Author’s Visuals)

Although Shopify shines in terms of revenue growth, other players such as Wix, Squarespace and Block also still have very decent double-digit growth and are only trading at 20-29x EV/EBITDA multiples unlike Shopify, which is above 125. Even compared to other large software companies such as Salesforce (CRM) and Adobe (ADBE), which are only trading at 22-25x EV/EBITDA while having double-digit revenue growth. In short, we do not believe Shopify currently offers an investment opportunity at a reasonable price on a relative basis, even though we believe it is a great business model.

A Stretched Valuation

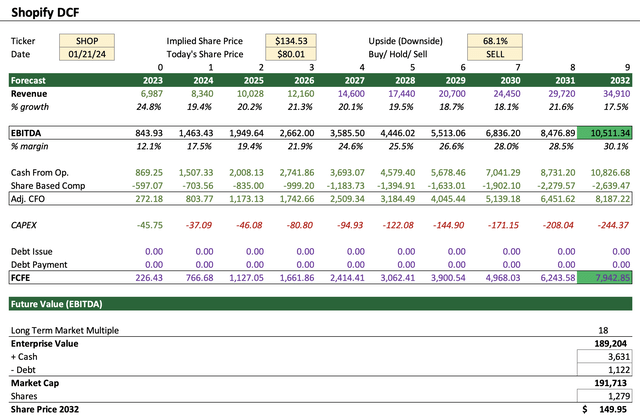

We have also re-run our DCF valuation with updated assumptions based on the above information, and we still cannot find value at current price levels. In terms of assumptions, we modeled revenue growth of about 20% over the next nine years, with EBITDA margins increasing to about 30%. For context, based on the last 12 months (LTM), Shopify saw average revenue growth of 20% in the last six quarters, with EBITDA margins peaking at 14.1% in the second quarter of 2021. In other words, in this valuation model, we expect Shopify to slow revenue growth only moderately while expanding EBITDA margins to more than double what they were last quarter.

This alone would be an incredible achievement if they succeed, in a very optimistic scenario. We think this is only possible if they are able to use their pricing levers excessively with customers without experiencing too much churn. Currently, the attach rate, or revenue generated as a proportion of gross merchandising value (GMV) is 3.05% compared to 2.96% the previous quarter. Although GMV growth may slow down over the forecast period, we believe that revenue growth of nearly 20% over the entire period is still possible with a higher attach rate considered, and we have modeled it accordingly. Just as the last subscription price increases worked out well, we believe the stickiness of Shopify’s platform may also justify a higher attach rate as they tie retailers into their ecosystem.

Author’s DCF

This leaves us in our very optimistic scenario with $10.51 billion in EBITDA by 2032, with very generous margins of 30.1%. On a free cash flow basis, we corrected for the heavy share-based compensation and modeled this to the end of the period, leaving us after CAPEX with free cash flow to equity (FCFE) of $7.94 billion. On an EV/EBITDA basis, at a multiple of 18x, that gives us $149.95 per share at the end of the period.

Looking at it on an FCFE basis, we think Shopify could potentially generate $6.21 in FCFE per share at the end of the projected period, which at a 5% FCFE yield or a 20x multiple comes out to $124.25 per share.

Author’s DCF

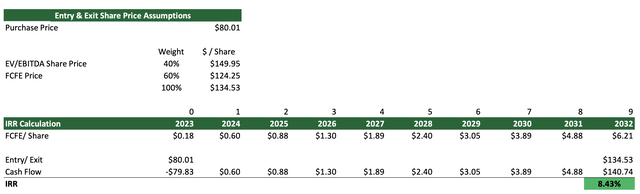

Taking both valuations into account, we lean slightly more heavily on the FCFE valuation with a weighting of 60%, given Shopify’s tendency to lean fairly heavily on stock-based compensation. Next, we take our combined price target of $134.53 and the price per share of $80.01 that Shopify is currently trading at and put it into an Internal Rate of Return (IRR) calculator. This gives us an IRR of 8.43%, which we believe is a very optimistic scenario and well below our minimum threshold of 10%.

Author’s DCF

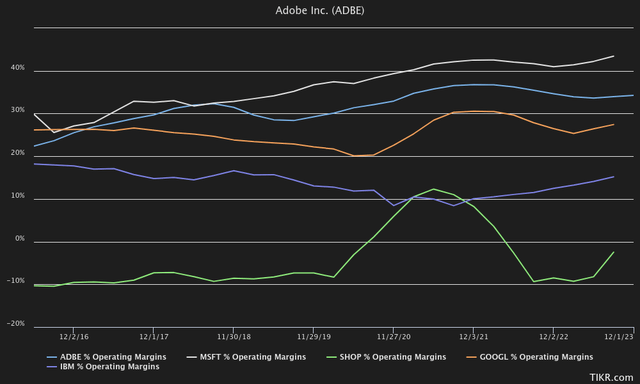

In conclusion, the only way we see Shopify’s valuation coming to fruition is if it performs some sort of miraculous feat by either beating revenue growth near 20% or growing margins above 30%, closer to the 52.6% gross margins it currently has. Only a small number of large software companies, such as Adobe and Microsoft, have operating margins approaching 40%. While it is possible, we see it as a huge gamble at this point.

TIKR Terminal

The Bottom Line

Although we could see great value in Shopify around the $29 price point in October 2022, we believe the current valuation is too high on both a relative and absolute basis, even with optimistic assumptions. While Shopify has a tremendous business model with very sticky revenues, it will take near-perfect execution to justify the current valuation.

We still believe Shopify is a great player in the field of AI and still has a lot of growth prospects in the B2B market and may become a great investment again if it drops to a lower price level, closer to $52 last year when we gave the stock a “Hold” rating. We are changing this rating to a “Sell” rating as we believe it is time to start unwinding the investment and wait for better entry opportunities at lower prices.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here