Thesis

The ETC 6 Meridian Hedged Equity-Index Option Strategy ETF (NYSEARCA:SIXH) is an equity exchange-traded fund. As per its literature:

SIXH seeks to provide capital appreciation. To achieve this objective, the fund pairs a portfolio of equity securities with an index call option writing strategy designed to reduce the exposure of the fund to broad equity market risk with the goal of providing strong risk-adjusted returns.

The fund contains a portfolio of large cap equities while at the same time writing covered calls on the S&P 500 index. SIXH is an actively managed ETF, and has flexibility in terms of establishing the ratio of written calls to its portfolio. Furthermore, the fund has a wide mandate, with the manager being able to short the market via inverse ETFs if such a decision is made. The vehicle is thus able to protect returns during downturns as compared to traditional buy-write funds.

In this article, we are going to take a closer look at SIXH, its build, historic performance in bull and bear cycles, and show retail investors why the fund is an attractive proposition in today’s environment.

Portfolio build – an active approach

Unlike traditional buy-write ETFs or CEFs which contain the same equities as the S&P 500 index, SIXH has an active construction approach which focuses on the best quality stocks with momentum:

Portfolio Mechanics (Fund Website)

In constructing the equity portion of the portfolio, the fund utilizes a three-step process to select securities to be held, as outlined in the above chart. Low momentum and low-quality names are eliminated first, with the second step of the process geared towards the ranking of the remaining population. The managers utilize a proprietary algorithm to screen for the above factors.

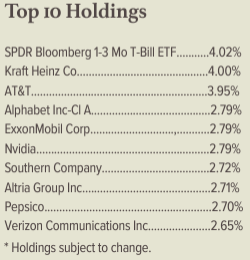

The end result is a portfolio of 51 equities, with the following top holdings:

Top Holdings (Fund Fact Sheet)

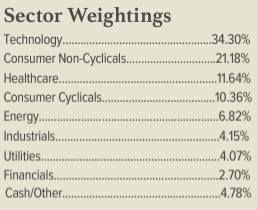

From a sectoral standpoint, the current portfolio is overweight technology names:

Sectors (Fund Fact Sheet)

Technology represents 34.3% of the portfolio, followed by Non-Cyclical Consumer at 21.1% and Healthcare at 11.6%.

Currently, the fund has only a small portion of its portfolio overwritten via covered calls:

Covered Calls (Fund Website)

The fund sold 780 SPX contracts, with a June 21 maturity date and a strike of 5200. As the index has already passed the strike level, the written calls are now in the money.

The fund’s active approach to portfolio construction is a significant positive for the vehicle, since it is able to identify momentum names, and thus capture more of the upside versus a passive reconstruction of the S&P 500. We also like the feature of being able to lower the portfolio delta via inverse ETFs if the managers deem necessary.

Analytics

- AUM: 0.4 billion

- Sharpe Ratio: 0.62 (3Y)

- Std. Deviation: 10.6 (3Y)

- Yield: 1.88% (30-day SEC yield)

- Premium/Discount to NAV: n/a

- Z-Stat: n/a

- Leverage Ratio: 0%

- Effective Duration: n/a

- Composition: Buy-Write Equities – Active Management

Performance – ideal fund for risk-off markets

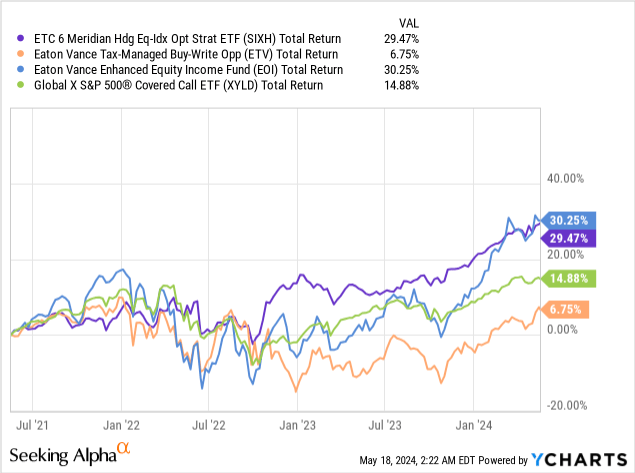

The fund has outperformed in the past three years, being a robust tool to use during market downturns:

We are comparing the name with the Eaton Vance Tax-Managed Buy-Write CEF (ETV), the Eaton Vance Enhanced Equity Income Fund (EOI) and the Global X S&P 500 Covered Call ETF (XYLD). All funds (be it CEF or ETF) utilize a covered call strategy to extract dividends from the S&P 500.

Since the start of the Fed hiking cycle in 2022, the market has experienced several downturns, with the most notable one in October 2022. We can see from the above graph that SIXH has navigated the macro set-up best, having the lowest drawdown, but yet the same upside as the SPY (EOI is utilized as a proxy here since it has the same total return profile).

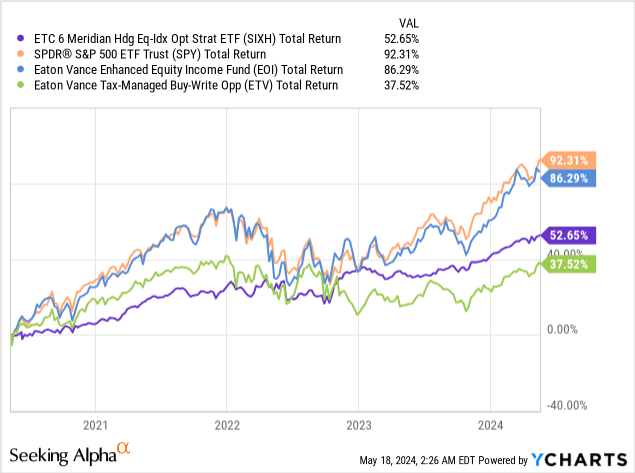

During cyclical bull markets, however, SIXH lags:

On a longer time-frame, SIXH lags, highlighting the upside given up via its written calls feature. The fund is thus a preferred choice during a bear market or for investors looking to position themselves conservatively, while the instrument will lag during cyclical bull markets. Nonetheless, it is interesting to note that on a 5-year time-frame, the fund has managed to beat the much better known Eaton Vance Tax-Managed Buy-Write Fund (ETV).

Not a high-yielding instrument

Unlike CEFs or other buy-write ETFs, SIXH is not structurally set-up to provide for a high yield. The vehicle has a 1.88% 30-day SEC yield, versus 9% for ETV. Traditional buy-write funds aim to extract dividends from the equity market via the overlaid written calls. As the calls expire, the option premium is used as a distribution tool as applicable.

Conversely, SIXH aims to provide capital appreciation, thus its market price and NAV are increased in those instances where the written calls expire without being triggered. An investor looking for high yield from equities is not well served by SIXH.

The fund has a monthly dividend payout, which you can find on the Seeking Alpha Dividend History tab.

Why is SIXH attractive at this stage

SIXH falls in the ‘conservative’ buy-write ETF category via its build. Unlike systematic vehicles like ETV, SIXH is actively managed and flexible in its approach in overlaying covered calls. This flexibility mainly stems from the fact the instrument is not set up as a high-yielding tool; thus, the fund does not have the pressure of utilizing calls when analytics are not attractive.

Furthermore, the fund is able to lower the portfolio delta via inverse ETFs when it deems necessary, a feature which has helped the name achieve a low -11% drawdown during the past three years, as compared to a -22% figure for the SPY and most buy-write vehicles in the market.

As the current set-up attests, the fund also captures the upside dynamically, with the current portfolio having only a very small proportion overwritten with calls. As the market rallies, SIXH will outperform versus constrained vehicles.

Conclusion

SIXH is an actively managed buy-write ETF, with a very wide mandate. The fund employs a proprietary strategy to build a portfolio of equities, screening for momentum and value. The resulting pool of assets is overlaid with covered calls to the extent the manager deems attractive given VIX levels and market dynamics. The fund also has the ability to overlay the portfolio with inverse ETFs if necessary. SIXH is set up for capital appreciation, not dividend yield, thus being different from competing buy-write ETFs or CEFs.

SIXH has been an outperformer in the past three years, almost matching the S&P 500 performance, but with only half the volatility. The fund is an attractive proposal for today’s market via its active approach to managing its downside, and its ability to employ inverse ETFs to decrease risk as applicable.

Read the full article here