")

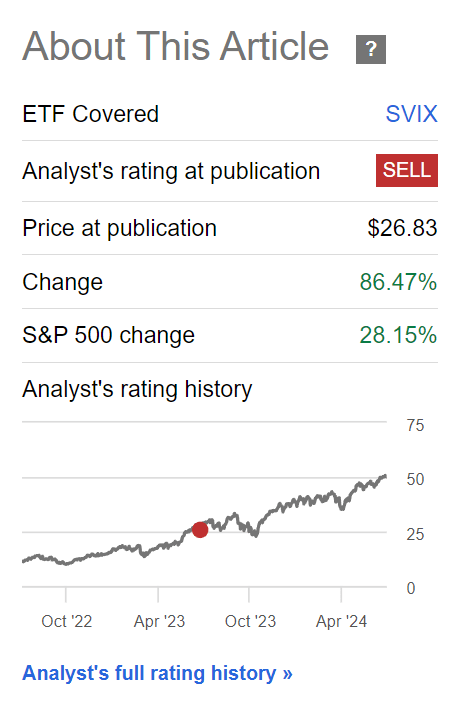

There is no question that short volatility strategies have been an incredible trade in the past year. Measured from my ill-timed recommendation for investors in the -1x Short VIX Futures ETF (BATS:SVIX) to take profits in July, the SVIX ETF has returned an incredible 86%, more than triple that of the S&P 500 Index (Figure 1).

Figure 1 – SVIX has tripled S&P 500’s returns since July 2023 (Seeking Alpha)

However, investors in the SVIX ETF were literally an inch away from a potential Volmageddon 2.0 event this past weekend, when former President Trump was nearly assassinated at a campaign rally in Butler, Pennsylvania.

Looking forward, the VIX index historically rises in election years from mid-July to end-September, which could act as a headwind for the SVIX ETF. Furthermore, as former President Trump’s election odds rise, investors may have to start factoring in potentially higher inflation, larger deficits, and trade wars. I urge SVIX investors to consider taking profits ahead of an expected rise in volatility.

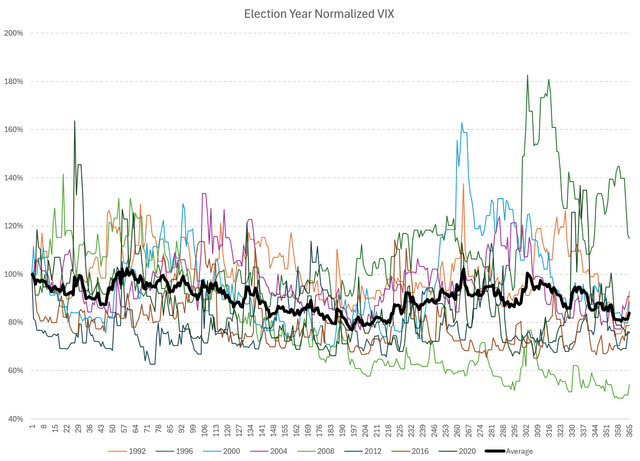

Election Year Volatility Set To Rise

Historically, if we look at volatility during presidential election year volatilities, the VIX index tends to bottom around day 196 (mid-July) and peaks on day 264 (end-September) (Figure 2).

Figure 2 – Normalized VIX seasonality in election years (Author created with data from St. Louis Fed)

This pattern in volatility is relatively easy to understand. Taking this year’s election as an example, we are seeing increasingly acrimonious rhetoric from both political parties, culminating in the horrific attack this past weekend against former President Trump.

Looking ahead, although President Biden has condemned the attacks on former President Trump and has called for civility, the heated rhetoric is unlikely to cool off with both political parties entrenched in their views. Rising political uncertainty raises the probability of tail risks, which may act as a headwind for short-volatility funds like the SVIX.

Brief Fund Overview

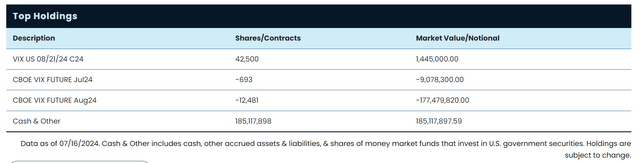

For those not familiar, the SVIX ETF holds a rolling short position in the first and second-month VIX futures that are rolled daily (Figure 3).

Figure 3 – SVIX portfolio holdings (volatilityshares.com)

The SVIX ETF has almost $190 million in AUM and charges a 1.47% net expense ratio.

Potential Trump Economic Policies Could Also Lead To Volatility

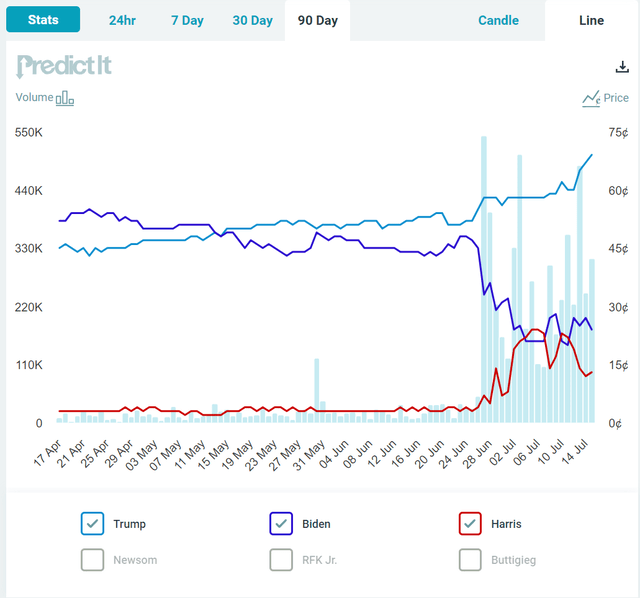

In addition to the risks directly associated with the election, as former President Trump’s re-election odds increase (Figure 4), investors may also begin to price in his economic policies.

Figure 4 – Rising odds of a Trump presidency (predictit.org)

As I have written previously, there is concern among mainstream economists that some of former President Trump’s policies may be inflationary and may counteract the Federal Reserve’s struggle to rein in inflation.

For example, one key campaign promise of former President Trump is his tough stance on immigration, with the former President stating he will direct law enforcement and the National Guard to deport millions of undocumented immigrants once he is re-elected.

While having a secure border is important, economists fear that tough immigration policies may inadvertently raise the barriers to legal immigration. With fewer immigrants, inflation could worsen, particularly in low-skilled service sector jobs.

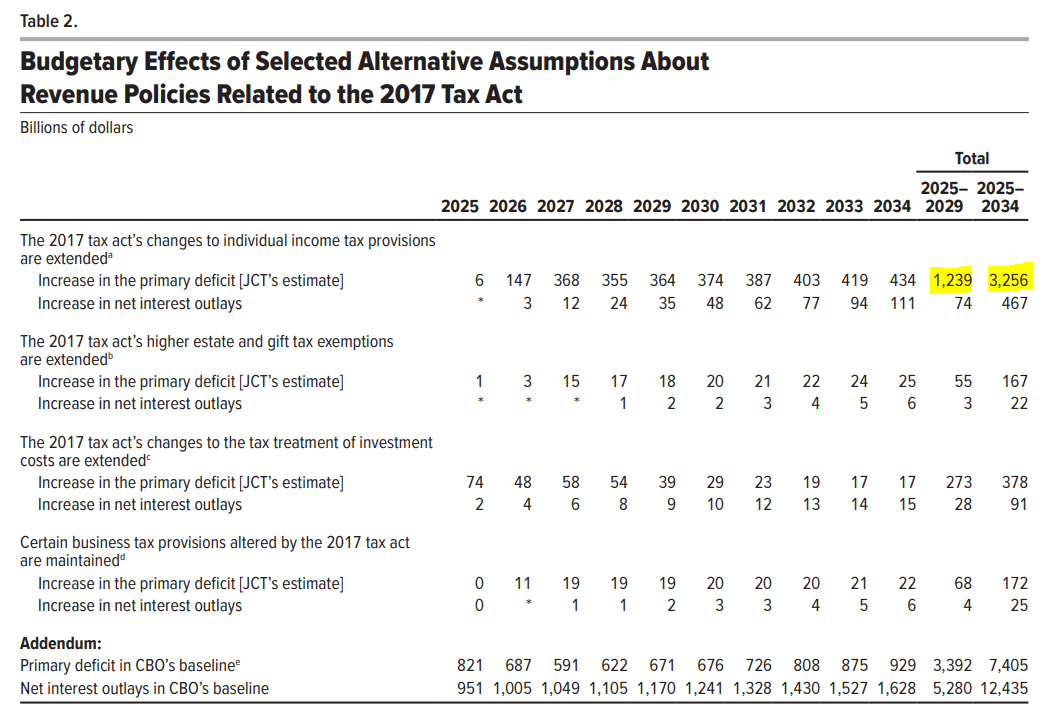

A second key Trump policy may be the extension of his signature tax breaks that are due to expire in 2025. According to the Congressional Budget Office (“CBO”), extending the Trump tax cuts for another 10 years – as Republicans have proposed – may add $4.6 trillion to the U.S. deficit in addition to higher interest expenses (Figure 5). This could worsen America’s unsustainable fiscal situation and lead to higher inflation.

Figure 5 – Extending Trump tax cuts could add $4.6 trillion to budget deficits (CBO)

Finally, let’s not forget that former President Trump famously nicknamed himself the Tariff Man, in a nod to the protectionist trade policies he enacted while in office. His trade war with China was partially responsible for a nearly 20% decline in the markets in 2018 before the Fed stepped in with interest rate cuts. He has vowed to increase tariffs on China if he is re-elected, and markets may see a replay of the 2018 drawdown.

Risks To Thesis

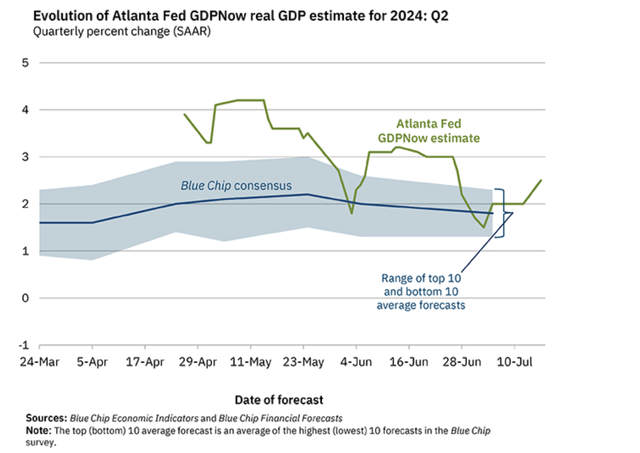

The risk to my cautious thesis is that volatility may remain subdued as economic growth continues at a moderate pace, with the Atlanta Fed estimating GDP growth of 2.5% for Q2/2024 (Figure 6).

Figure 6 – GDPNow growth forecast (Atlanta Fed)

Markets could also view Trump’s tax policies as ‘pro-growth’, which could outweigh the potential negatives.

Finally, raising trade barriers may spur domestic production capacity and lead to a renaissance in American jobs and income.

Conclusion

The SVIX ETF has had a great run as equity markets have climbed the ‘wall-of-worry’ in the past year and SVIX has delivered exceptional returns. However, looking forward, I believe short-volatility strategies like the SVIX may face headwinds as political uncertainty increases into the November election.

Furthermore, as investors begin to price in a potential Trump victory, they will have to start factoring in potential market headwinds from Trump’s economic policies such as higher inflation, larger deficits, and trade wars. I urge SVIX investors to exercise caution and consider taking profits. I reiterate my sell recommendation on SVIX.

Read the full article here