")

This article analyzes Synchronoss Technologies, Inc. (NASDAQ:SNCR) Q2 2024 results and the earnings call. It also reviews the company’s valuation since my last article in February.

Synchronoss’ results for the year were in line with guidance and expectations, delivering mid-single-digit top-line growth with good operating leverage after divestment in 2023. This operating leverage has led to the company recovering operating profitability, an important point given its high leverage.

On the capital stack side, the company repurchased its expensive 14% preferred stocks, replacing it with debt at SOFR + 550bps (11%), which is also expensive but less so. The company still carries significant debts ($180 million or 9x NOPAT).

From a valuation standpoint, the stock is moderately up from my last article, a development that seems logical given the fundamental improvements of the company. It currently trades at an expected P/E of 14x or an expected EV/NOPAT of 15x. In my opinion, none of these seem attractive given the company’s high leverage and competitive position.

Positive quarter

Synchronoss has improved significantly since it restructured its business last year. Margins have improved, and revenues are growing. Further, the company has restructured its debt this quarter, helping alleviate the weight of interest expenses.

Top line at MSD: The company grew 6% in 2Q24 and 4% in 1H24. This level of growth is expected for FY24, with guidance of 5% top-line growth. Synchronoss’ business grows with subscribers over time, which in turn depends mostly on people signing up for cloud storage services offered by mobile operators like Verizon. The company guides for mid double-digit growth over the coming years, but I believe this is very optimistic.

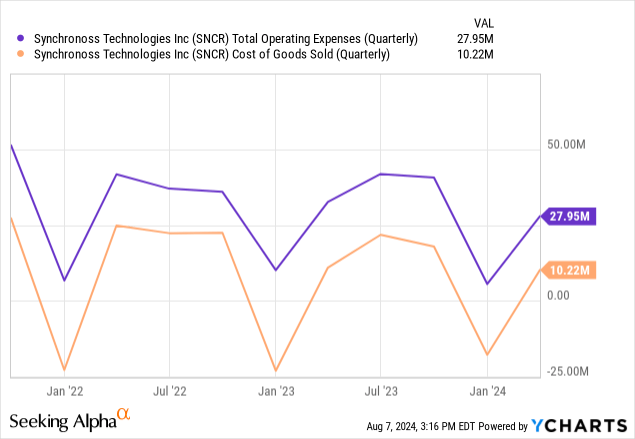

Cost leverage: The company’s main improvement has come from reducing its operating expenses, a big portion of the rationale behind divesting businesses last year. OpEx was down 15% both at the 2Q24 and 1H24 level. This has allowed the company to post operating income for 1H24 ($8.9 million) versus a loss last year.

Not many business developments: The company operates in a relatively steady state, with a few customers constituting the majority of its revenues and no control over user growth. The quarterly call made no mention of new product launches or customer gains, only the set-up of a new manager for the Japanese market.

Debt restructuring: Synchronoss fortunately bought back all of its preferred shares, which were yielding a high 14% and were not convertible. This was done via a term loan paying SOFR + 5.5%, which currently comes up to about 11%. This allows the company to save about $2 million a year in interest. As a reminder, the company also has notes outstanding for about $115 million, with a coupon of about 8.3%

The valuation is more interesting, but not attractive

Based on Synchronoss guidance, the company should generate about $172.5 million in revenues this year, or a growth of 5%. In addition, the company is expecting to post adjusted EBITDA margins of 30% over the long run (with no comments made about FY24). This leads to $52 million in adjusted EBITDA over the long-run, based on FY24 expected revenues.

From that figure, we need to remove between $15 and $20 million in CAPEX/D&A and another $5 million for SBC to reach an operating income of about $29 or $30 million. This is a significant improvement from the TTM $15 million when I wrote in March.

The improvement in the debt structure is also a positive. Based on a term loan of $75 million and $115 million in notes, we can expect interest of $17.75 million per year. If the company eventually receives the $28 million it is expecting from the IRS, its interest expenses should decrease to about $15 million per year.

After taxes of 25% (the company only has $20 million in federal NOLs), these figures result in an expected FY24 NOPAT of $21 million and a net income of $8.5 million. In both cases, it represents an EV/NOPAT or P/E of 14x to 15x or, conversely, a yield of 6.5%/7%. This seems relatively fair if the company continues growing at mid-single digits, reaching a yield of 12%. The IRS-based payment of debt could increase the earnings yield by another 3%, reaching potentially 15%.

However, I do not believe the above is an opportunity, as it requires the company’s revenues to grow MSD when the company has no control over that process (it cannot directly influence the users of its products). Further, Synchronoss Technologies, Inc. is still leveraged, and repaying the close to $200 million in debts it has would take a long time, even if income were to double from here.

Given the fundamental improvements, Synchronoss’ current valuation is more rational but not attractive for long-term holders. More speculative readers could consider it a bet on the company delivering on its promise to grow mid double digits, or in interest rates decreasing substantially.

I believe Synchronoss Technologies, Inc. is still a Hold after Q2 2024 results.

Read the full article here