")

It has been a year and a half since our last article on small-cap telehealth concern Talkspace, Inc. (NASDAQ:TALK). At the time, the shares were selling at just under the net cash on the company’s balance sheet, and Talkspace had just brought in new management. We concluded that piece with the recommendation that TALK seemed to a merit a small “watch item” position for aggressive investors. The equity has moved significantly higher since then, and the company posted its first quarter results five weeks ago. Therefore, it is a good time to circle back to Talkspace. An updated analysis follows below.

Seeking Alpha

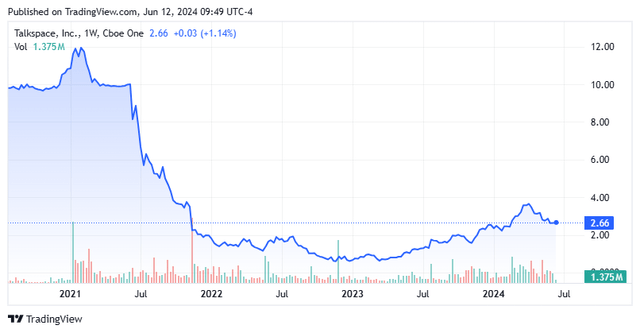

Talkspace is based out of the Big Apple. This virtual behavioral healthcare company provides psychotherapy and psychiatry services through its platform to individuals, enterprises, and health plans and employee assistance programs throughout the United States. The stock has moved to a bit over $2.50 a share and sports an approximate market capitalization of $445 million. The company was founded in 2012 and pioneered message-based therapy. It now has over 5,000 licensed clinicians that can address 150 conditions and treatment modalities.

Recent Results:

May 2024 Company Presentation

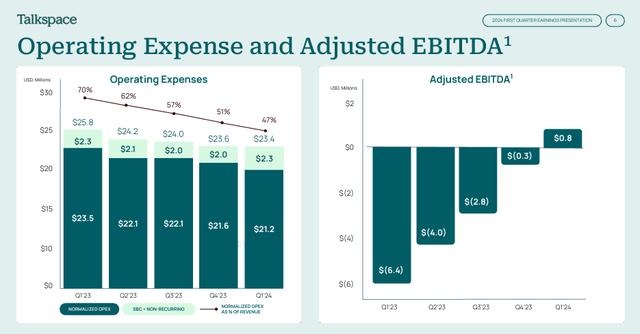

Talkspace posted its Q1 numbers on May 7th. The company delivered a GAAP loss of just a penny per share, as the net loss was just $1.5 million in the quarter. This is a significant and impressive improvement from the $8.8 million net loss in the same period a year ago. The company benefitted from a nine percent decrease in operating expenses from 1Q2023 to $23.4 million. Management credited efficiencies in its Research & Development and Clinical Operations for the expense reduction. Talkspace had Adjusted EBITDA of $800,000 in the quarter. It should be noted this is the first quarter the company has achieved positive Adjusted EBITDA.

May 2024 Company Presentation

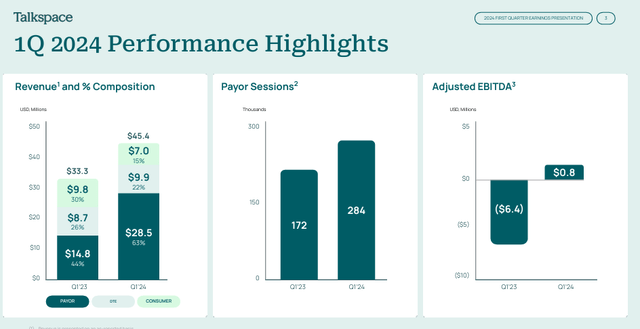

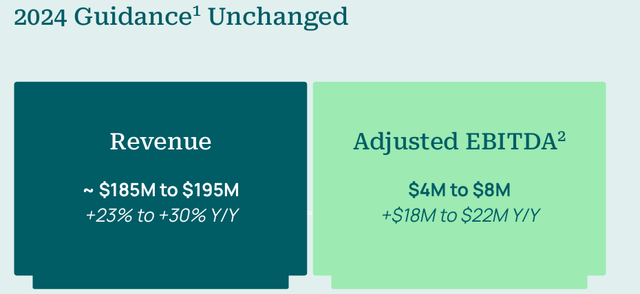

Revenues rose 36% on a year-over-year basis to a tad over $45.4 million. Eligible lives covered rose 34% to just over 131M, while the number of completed sessions rose 65% from the same period a year ago. Leadership maintained FY2024 sales guidance of $185 million to $195 million and expects to deliver $4 million to $8 million of positive Adjusted EBITDA for this fiscal year.

May 2024 Company Presentation

Of note, the company appointed a new CFO two weeks after Q1 results were posted. A week after first quarter numbers came out, Talkspace disclosed that it was expanding into the Medicare population and will offer virtual therapy services to approximately 13 million traditional Medicare members in eleven states.

Analyst Commentary & Balance Sheet:

The company gets sparse coverage from Wall Street despite a decent size market cap. Following Q1 results, TD Cowen reissued its Buy rating and $5 price target, while Barclays maintained its Hold rating with a $3 price target. Those are the only analyst firms I can find that have chimed in around Talkspace so far in 2024.

The company ended the first quarter with just over $120 million in cash and marketable securities on its balance sheet against no long-term debt, according to the 10-Q Talkspace filed for the quarter. Insiders are maintaining their stakes in the firm, and there have been no insider sales in this stock since September 2022.

Conclusion:

The company lost 12 cents a share in FY2023 on $150 million in sales. The current analyst firm consensus has Talkspace losing just a penny a share in FY2024 as revenues move close to $190 million. They project a nickel a share profit in FY2025 on revenue growth of 18%.

Talkspace, Inc. has executed quite well since we last looked at the company. While now yet profitable on a full-year basis, it is rapidly moving in that direction. Given sales growth, the stock is not overpriced at just over 2.3 times forward sales. Adjusting for the net cash on the company’s balance sheet, the equity sells for roughly 1.7 times forward revenues.

Therefore, I am going to maintain my small holding in Talkspace, Inc. stock, and will look to accumulate additional shares during any decent dip in the overall market.

Read the full article here