")

Founded in 1976, The Duckhorn Portfolio (NYSE:NAPA) operates a portfolio of wine brands throughout North America. The company’s brands include names such as Duckhorn Vineyards, Paraduxx, Decoy, Goldeneye, and Migration. Duckhorn gets the majority of revenues through wholesale, but also sells wine directly to customers.

After an IPO in early 2021, Duckhorn’s stock has nearly halved in price stably despite quite a good earnings trajectory from the IPO figures.

Stock Chart From IPO (Seeking Alpha)

A Track Record of Profitable Growth

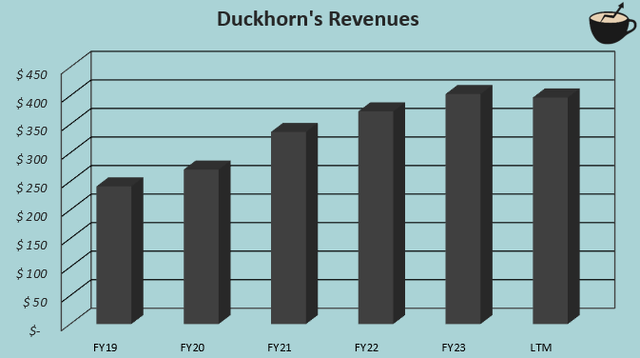

Duckhorn has had a revenue CAGR of 11.7% from FY2019 to current trailing revenues as of Q2/FY2024. The company has been able to stably increase sales with a portfolio of luxury wines. With the stable growth, Duckhorn has also been able to keep up very great margins; the company currently has a trailing operating margin of 26.1%, within the upper range company’s historical annual range of 23.0% to 27.0% from FY2019 to the current trailing margin.

Author’s Calculation Using Seeking Alpha Data

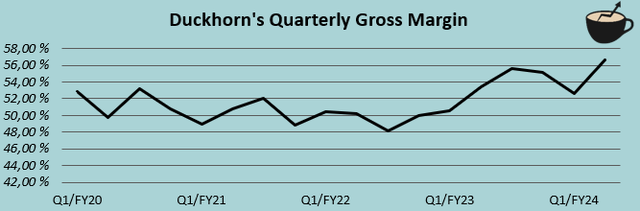

Duckhorn boasts great margin expansion in the company’s Q2 investor presentation, where Duckhorn communicates a great sourcing of grapes as a driver of greater margins. In Q2/FY2024, the company’s gross margin expanded from 53.3% into 56.6% from Q2/FY2023, resulting in an operating margin expansion of 3.4 percentage points year-over-year. The company has started to expand the gross margin quite clearly on a quarterly basis.

Author’s Calculation Using TIKR Data

While the margin expansion is great, I don’t see it reasonable to extrapolate the margin expansion too much for the time being; even with the higher gross margin level, Duckhorn’s operating margin still stands within the company’s historical range.

The Growth Requires Capital

The growth hasn’t come without capital requirements – Duckhorn has had a good amount of investments. In Q4/FY2023, the company acquired a wine production facility in California, increasing capital expenditures by around $55 million in the quarter. Continuous growth requires such investments in capacity expansion. Another significant capital requirement is constant working capital growth; Duckhorn has had to expand inventories to support the growth, now growing inventories by $62.7 million in the past twelve months and expanding total working capital by $78.4 million. The company’s working capital has increased on a constant basis to support growth.

With capital expenditures and working capital changes combined, Duckhorn’s cash flows are currently quite hindered. The company has a current trailing return on equity of 7.01% as per Seeking Alpha’s profitability data, and while the return on equity is higher at around 11.96% when excluding goodwill, the growth certainly isn’t free. The achieved return on capital is fairly good, but doesn’t make the growth exceptionally valuable.

Current Weakness

As can be seen from recent quarters’ revenues, Duckhorn’s revenues haven’t grown in FY2024 so far within the first half of the fiscal year. The first half has shown a year-over-year revenue decline of -2.9% mostly due to a weak Q1. Duckhorn relates the weakness to a weakly performing industry in the company’s Q1 earnings call, as the consumer sentiment has been soft.

Duckhorn already narrowed the FY2024 revenue outlook range into the lower bound with the Q1 report, and further decreased the revenue outlook with Q2 earnings; the current guidance of $395 million to $411 million in revenues could still see some pressure downwards. The current guidance’s middle point still expects some revenue growth in the second half of the year. Duckhorn told that the company expects the market to stay challenging in upcoming quarters in the Q2 earnings call, but still expects to beat the overall luxury wine market in growth. In the Q2 investor presentation, Duckhorn shows a growth of 3.0% for the company in the twelve weeks ending on 01.28.2024 compared to a luxury wine performance of 1.1%; the current hiccup in growth seems very likely to subside eventually, and isn’t representative of a poor company-specific performance but rather a weak market.

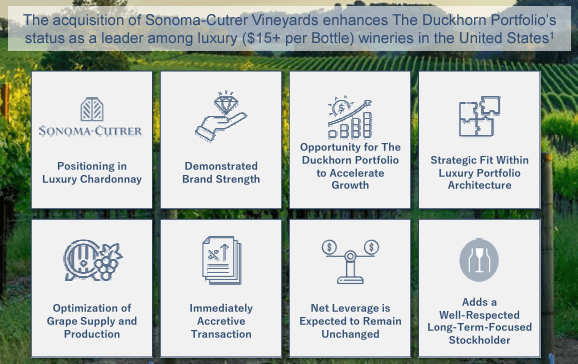

Acquisition of Sonoma-Cutrer Vineyards

Duckhorn announced the acquisition of Sonoma-Cutrer Vineyards in November of 2023, to be purchased from Brown-Forman, a company of which I have previously done a write-up on. The acquisition is to be made with a total consideration of around $400 million, including 31.5 million Duckhorn stock amounting to $350 million at the time of the deal, as well as a cash consideration of around $50 million with certain unspecified adjustments. The acquisition is to be completed in the spring of 2024.

The acquired company had around $84 million in sales in the fiscal year ended on the 31st of July in 2023. With the current stock valuation, the price tag comes up to $333.5 million, representing an EV/S ratio of 3.97 compared to Duckhorn’s current trailing EV/S of 3.35; the acquisition wasn’t made at a very attractive price in comparison to Duckhorn’s own valuation. Sonoma-Cutler Vineyards was mentioned to have a similar adjusted EBITDA margin as Duckhorn. The expected annual run-rate synergies of $5 million make the acquisition reasonably valued in my opinion, though. Duckhorn further rationalizes the acquisition with an improved positioning in luxury Chardonnay.

Duckhorn Q2 Investor Presentation

Share Fall Now Represents an Attractive Entry Point

Although Duckhorn was initially trading at a high P/E after the IPO, good earnings growth and a lower stock price have attributed into a currently more attractive forward P/E multiple of 14.1.

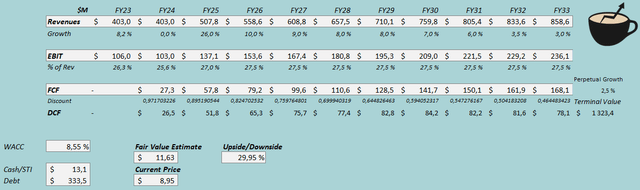

To further demonstrate the valuation, I constructed a discounted cash flow model. In the DCF model, I factor in the acquisition of Sonoma-Cutrer Vineyards with a higher share count by 31.5 million, as well as $50 million more in debt. To demonstrate more clearly, I estimate the acquisition to be accretive to earnings starting in FY2025, creating a growth of 26% for the year after stable revenues in FY2024. Afterwards, I estimate growth that’s roughly in line with Duckhorn’s demonstrated history with an estimated 10% for FY2026, slowing down gradually into a perpetual growth rate of 2.5% and representing a total revenue CAGR of 6.8% from FY2025 into FY2033 with an organic performance.

With the acquisition’s similar adjusted EBITDA margin, but anticipated $5 million synergies and demonstrated gross margin leverage, I estimate Duckhorn’s EBIT margin to rise from an estimated 25.6% in FY2024 into 27.5%, representing some leverage. The company’s growth requires quite a ton of capital, and I estimate the cash flow conversion as poor initially, but improving as the growth slows down.

With the mentioned estimates along with a cost of capital of 8.55%, the DCF model estimates Duckhorn’s fair value at $11.63, around 30% above the stock price at the time of writing. After the stock’s slope downwards, the current price now seems to represent quite an attractive entry point.

DCF Model (Author’s Calculation)

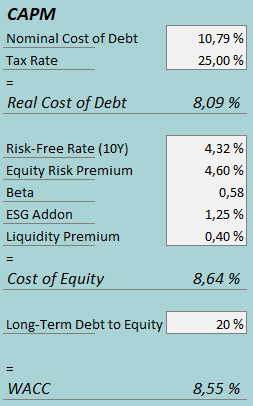

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

With Duckhorn’s current interest-bearing debt and Q2 interest expenses, the company’s interest rate comes up to quite a high figure of 10.79%. The company leverages debt quite well, and I estimate the long-term debt-to-equity ratio to stand at 20%, slightly lower than currently. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.32%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Duckhorn’s beta at a figure of 0.25. I believe that the estimate is very low, and instead use the average of three other alcohol producers in addition to Duckhorn’s beta – along with Brown-Forman’s beta of 0.79, Constellation Brands’ beta of 0.96, and Diageo’s beta of 0.33, a beta of 0.58 is created. Finally, I add a small liquidity premium of 0.4%, creating a cost of equity of 8.64% and a WACC of 8.55%.

Takeaway

Duckhorn has grown earnings steadily in the past few years. In addition, the company reports constantly high margins with improved gross margins signifying slight margin expansion potential in challenging market conditions that have overall contributed negatively into recent quarters’ growth. Although the growth doesn’t come free with investments in a new facility, increased inventory needs, and acquired growth, I believe the stock price reflects quite an attractive entry point after the stock’s steady fall. My DCF model estimates quite a good amount of upside for the stock; for the time being, I believe that a buy rating is constituted.

Read the full article here