")

Whirlpool Corporation (NYSE:WHR) is one of the most well-known brands among household appliances. From fridges through washers and dryers to ice makers, WHR manufactures and sells a wide variety of products.

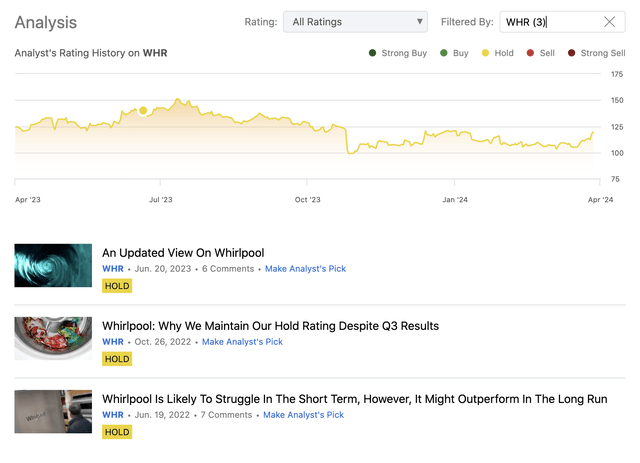

We have already published three articles about WHR and its business since the start of our coverage in June 2022. Each time, we have assigned a neutral “hold” rating to the company’s stock. Let us recap our main arguments for the neutral ratings:

- Macroeconomic headwinds in 2022 and 2023, mainly driven by poor consumer confidence and elevated inflation levels

- These headwinds eventually led to poor financial performance in these past years

- On the other hand, the firm has been a reliable dividend payer and has also engaged extensively in share buybacks

Analysis history (Author)

Our goal here is to give an updated view, both on a macro- and microeconomic level and assess whether our previous neutral rating is still justified or maybe an upgrade/downgrade is necessary. We will be examining the firm’s last quarterly results, its valuation based on price multiples and its return to shareholders over time.

Quarterly results and its implications – January 2024

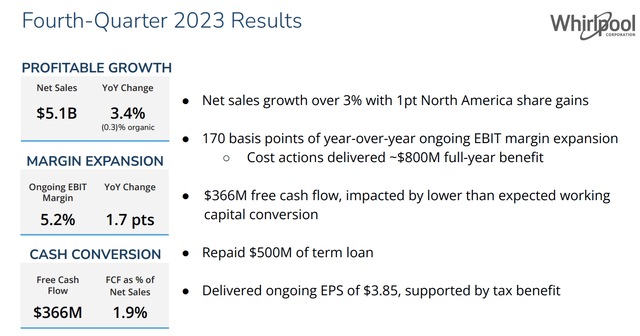

For the last quarter of 2023, the firm has reported an increase of 3% in net sales, although organic sales have declined slightly by 0.3%. This improvement has been accompanied by an expansion in both the operating margin and the net income margin. The firm’s $800 million cost reduction has been one of the key drivers of this improvement. A tax benefit in the prior year has also had a positive impact on the bottom line results.

Looking ahead to 2024, the company’s forecasts do not foresee a significant growth in terms of GAAP and ongoing earnings per diluted share. These are expected to be in the ranges of $8.50 to $10.50 and $13.00 to $15.00, respectively, with expected cash provided by operating activities of $1.15 to $1.25 billion. On the other hand, a significant improvement is anticipated in terms of free cash flow, which is expected to be in the range of $550 to $650 million.

Q4 results (WHR)

While we believe that these results are not extraordinary in any way, we would like to highlight a few points that we actually like:

Reduction of debt

We continue to create balance sheet flexibility and prioritize debt reduction with $500 million repayment of debt in 2023.

In our view, reducing debt in the current market environment is key. As the macroeconomic environment remains uncertain and interest rates are still at high levels, reducing debt can contribute significantly to the financial flexibility of the firm. Such actions are also likely to have a positive impact on the bottom line results, due to the reduced interest expenses, as well as on the firm’s liquidity ratios.

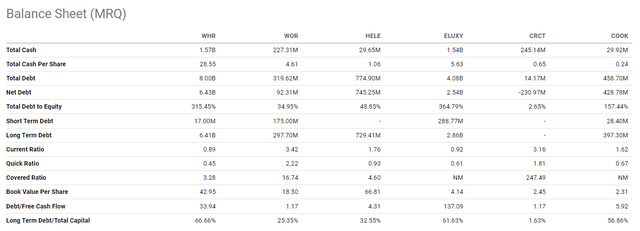

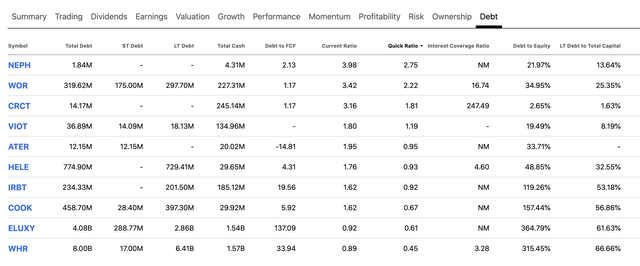

The following tables show how WHR’s debt level and liquidity compares with those of its peers.

Balance sheet (Seeking Alpha)

Comparison (Seeking Alpha)

Based on these, we can see that WHR’s business was by far not the most attractive, rather one of the least attractive ones, therefore we are delighted now to see that management has taken the decision and also the action to change this. We believe that this is the right course of action.

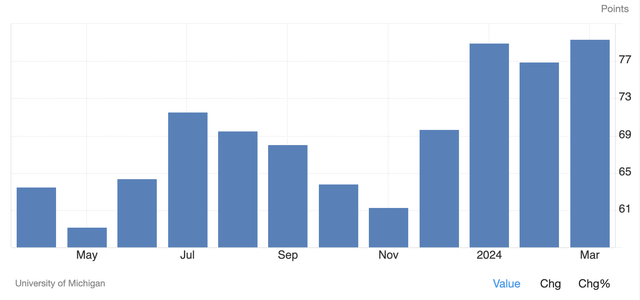

Improving consumer confidence

In the past months, consumer confidence in the United States has been gradually improving. While it is still well below the pre-pandemic levels, it is significantly higher than it was a year ago.

U.S. Consumer confidence (tradingeconomics.com)

As the consumer confidence is a leading economic indicator, we do not expect to feel the potential positive impacts until later this year. However, in general, we believe that the improving sentiment is likely to lead to more spending on discretionary, non-essential, durable products, which may benefit WHR’s business.

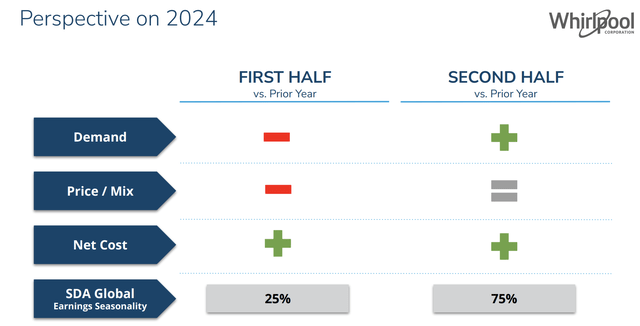

This development is also expected by the firm.

Perspective (WHR)

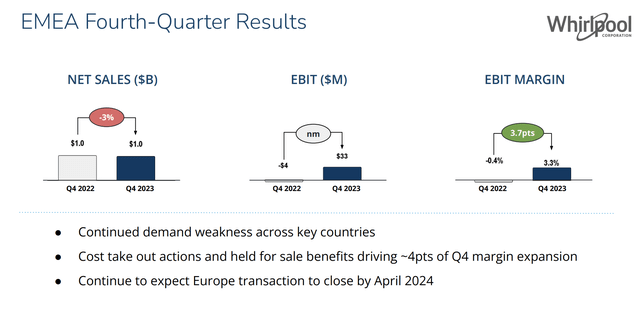

Europe transformation

The demand in Europe has been lagging, sales have been declining and the margins have not been extraordinary either. For these reasons, we believe the transformation of the business in this segment is justified and necessary.

EMEA results (WHR)

The Company expects the Europe transaction to close by April 2024, and full year guidance includes three months MDA Europe expected results (approximately $700 million of net sales and EBIT(4) margin of approximately 1.5%)

Return to shareholders

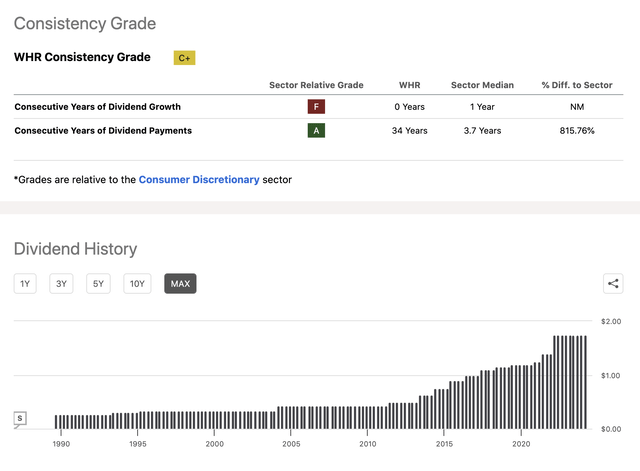

Whirlpool remains a reliable dividend payer with recently declaring a quarterly common dividend of $1.75 per share. This has been the ninth consecutive $1.75 dividend declaration, therefore we cannot really be happy about dividend growth. Dividend payments totaled $384 million in 2023.

Dividend history (Seeking Alpha)

On the other hand, there are other priorities right now in capital allocation, which we believe are more crucial, e.g. the reduction of debt.

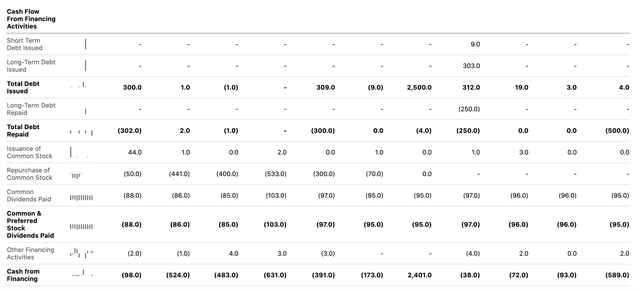

Further, the firm has been also pausing its share repurchases.

Cash flow from financing activities (Seeking Alpha)

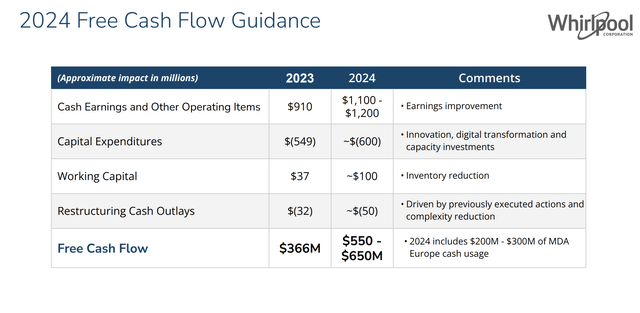

Before we move onto our next section, we have to emphasize that the current dividend appears to be safe and sustainable in the near future, as the firm’s free cash flow significantly exceeds the amount spent on dividends, and FCF is also forecasted to increase in the coming year.

FCF guidance (WHR)

All in all, we believe that for long term investors the firm’s capital allocation strategy is justified, and in our view, once the required debt reduction is achieved, WHR will once again start increasing its dividend and engage in share repurchases.

Valuation

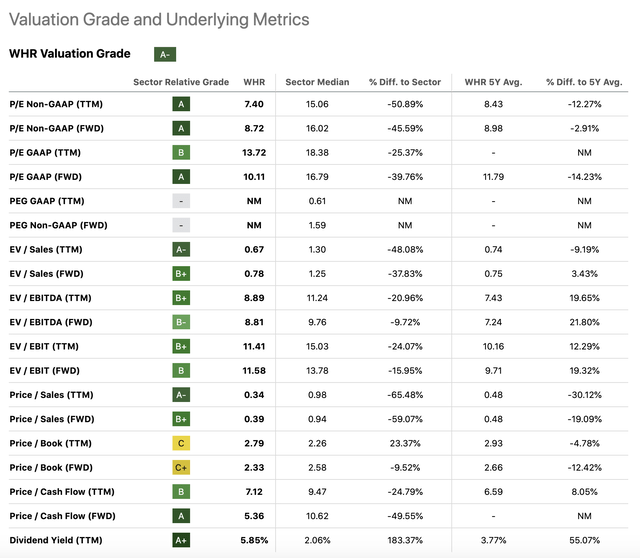

Today we will be looking at WHR’s valuation based on a set of traditional price multiples.

Valuation (Seeking Alpha)

While we believe that the growth of the firm and the recent financial results are not particularly attractive, the initiatives related to debt reduction and the transformation related to the European segment are promising. Considering that the firm is selling at a significant discount compared to the consumer discretionary sector, and also compared to its own historic valuation, based on several metrics, we believe that the current price could be an attractive entry point. In our opinion, the likely improvement in margins and the likely reduction in interest expenses justify the current valuation.

For these reasons, we are turning bullish from a valuation point of view.

Conclusion

While WHR has not delivered particularly strong results in Q4, there are several topics that give positive indication about the future. These include, improving consumer confidence, debt reduction initiatives and the transformation of the European segment.

The firm has shifted its capital allocation priorities to debt reduction from return to shareholders, which we believe is justified and could unlock value for long term investors. Regardless, WHR keeps paying a sustainable quarterly dividend.

From a valuation point of view, WHR also appears relatively attractive, considering the above mentioned initiatives, and the almost 6% dividend yield.

For these reasons, we upgrade from “hold” to “buy”.

Read the full article here